The market sentiments were dampened by the escalated India-Pakistan tensions, but the losses were restricted to 1.1 percent on the benchmark indices for the week ended May 9 amid hope that there won't be war-like situation. Healthy FII inflow in the last four weeks, record GST collections in April along with subdued US dollar and stable oil prices provided support to the market.

The market is expected to consolidate further with focus on corporate earnings, and inflation numbers by India and US. The announcement of ceasefire by both countries may lift sentiment but the caution will prevail until the end of uncertainty with respect to India-Pakistan tensions, according to experts.

The Nifty 50 was down 339 points (1.39 percent) to 24,008, and the BSE Sensex fell 1,047.5 points (1.3 percent) to 79,454.5, while the Nifty Midcap 100 index declined 0.9 percent and Smallcap 100 index dropped 2.2 percent.

Looking ahead, "markets will closely monitor key domestic macroeconomic indicators, CPI and WPI inflation data. The consensus anticipates a potential softening in inflationary pressures," Vinod Nair, Head of Research at Geojit Investments said.

However, according to him, geopolitical tensions between India and Pakistan remain a point of concern in the near-term.

Here are 10 key factors to watch next week:

India-Pakistan Tension

The market participants will keep an eye on further developments with respect to geopolitical tension between India-Pakistan. After the recent escalation of military action and severe attack by Indian army forces in several areas of Pakistan including nine terror hubs, both countries - India and Pakistan - have agreed to a temporary halt in all firings and military action on land, air and sea effective 5 pm on May 10, though there were reports of ceasefire violations. The meeting between Directors General of Military Operations (DGMOs) of both nations is scheduled to be held on May 12 to implement the agreed ceasefire and discuss measures to reduce tensions along the border.

Apart for geopolitical tension, investor will continue to focus on the ongoing March quarter earnings season as more than 500 companies will release their quarterly earnings scorecard including key companies like Tata Steel, Bharti Airtel, Hero MotoCorp, Eicher Motors, and Tata Motors.

Among others, Bharti Hexacom, Bajaj Electricals, PB Fintech, Jyothy Labs, PVR Inox, UPL, Zaggle Prepaid Ocean Services, Cipla, GAIL (India), Metropolis Healthcare, Siemens, Apollo Tyres, Berger Paints India, Hindustan Aeronautics, Jubilant FoodWorks, Lupin, Muthoot Finance, Shree Cement, Tata Power Company, Torrent Power, ITC Hotels, JSW Energy, LIC Housing Finance, Bharat Heavy Electricals, Delhivery, Emami, Hyundai Motor India, and Divis Laboratories will also release their numbers next week.

CPI Inflation

Additionally, key macroeconomic indicators such as Consumer Price Index (CPI) and Wholesale Price Index (WPI) numbers for April (which scheduled on May 13 and May 14 respectively) will also be closely watched to know about further path of RBI with respect to interest rate decision. According to economists, CPI inflation is expected to fall further in April, from 3.34 percent seen in March month.

Further, balance of trade data for April month will be released on May 15, and foreign exchange reserves for week ended May 9 on May 16.

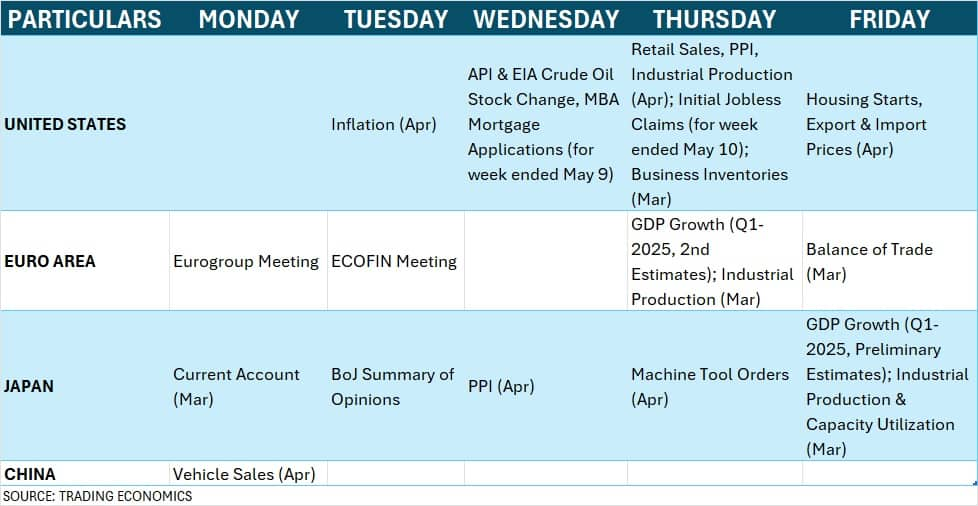

Global Economic Data

On the global front, the market participants will focus on the possible US-China discussions to finalise the trade deal between both countries by defusing a trade war that is disrupting the global economy.

Apart from that, the focus will also be on the estimates for GDP numbers for Q1-2025 from Eurozone and Japan which are scheduled next week.

Further, the industrial production, retail sales, PPI, and inflation numbers for April by the United States will also be closely tracked for insights into the economic outlook of the world's largest country.

Fed Chair Powell Speech

Globally investors will also focus on the speech by the US Federal Reserve Chair Jerome Powell on May 15. In the last week's policy meeting, the Federal Reserve has warned of stagflation risks. "So hotter-than-expected inflation coupled with weaker retail sales could further reduce the likelihood of near-term rate cuts," Kaynat Chainwala of Kotak Securities said.

The FII activity will also be keenly watched as the foreign institutional investors (FIIs) remained net buyers to the tune of Rs 5,087 crore in the cash segment last week despite sell-off on Friday, continuing buying for fourth consecutive week. They provided strong support to the market which recorded healthy rally before witnessing small profit booking last week.

Domestic institutional investors have net bought Rs 10,451 crore worth shares last week and Rs 13,741 crore for current month, which is better than FIIs inflow.

Meanwhile, the US dollar index managed to close above 100 mark for another week after rangebound trading, but is still far lower from its swing high of January (110.18).

On the primary market front, the mainboard segment will remain silent for the second consecutive week, but the action will continue in the SME segment with two new IPOs launching next week. Civil contractor Integrity Infrabuild Developers will open its Rs 12-crore IPO on May 13, and the Rs 30-crore public issue of pharma company Accretion Pharmaceuticals will hit Dalal Street on May 14.

Virtual Galaxy Infotech will close its IPO on May 14, while Manoj Jewellers, and Srigee DLM will debut on the BSE SME on May 12.

Technical View

Technically, the Nifty 50 formed bearish candlestick pattern, resembling Bearish Engulfing kind of formation (not a classical one) on the weekly scale with above-average volumes, signalling some weakness but defended 24,000 on closing basis and the losses limited to just 1.4 percent despite escalation in India-Pakistan tension. It still seems to be in the range of 23,850-24,600. Experts advise caution given the geopolitical tension. Until the index defends 23,850, the bears may not gain major strength, and the consolidation is likely to continue in the upcoming sessions. The decisive close below 23,850 can open doors for 23,600-23,500 zone.

F&O Cues

The weekly derivative data suggested that the Nifty is expected to be in the range of 23,500-24,500 in the short term with immediate support of 23,800 and resistance at 24,300 zone.

On the Call side, the 25,000 strike holds the maximum Call open interest, followed by the 24,500 and 24,000 strikes, with the maximum Call writing at the 24,000 strike, and then the 24,100 and 25,000 strikes. On the Put front, the maximum open interest was placed at the 24,000 strike, followed by the 23,500 and 23,800 strikes, with the maximum Put writing at the 24,000 strike, and then the 24,100 and 24,050 strikes.

Meanwhile, the fear index, India VIX remained elevated for third consecutive week, indicating caution for bulls. It surged 18.5 percent during the week to 21.63 levels.

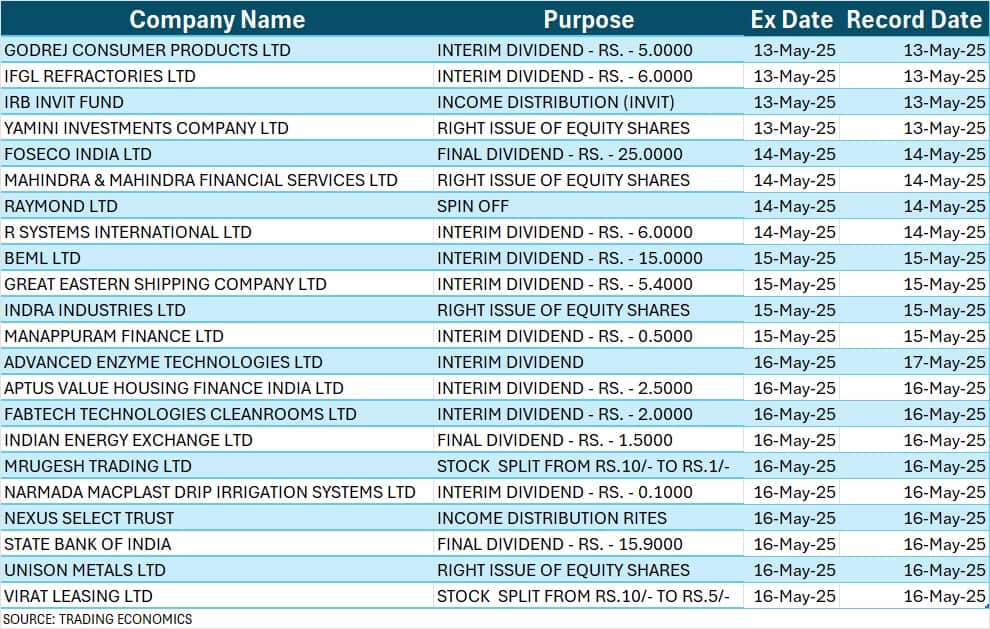

Corporate Action

Here are key corporate actions taking place in the coming week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.