The market staged strong performance in the week ended September 12, rising 1.5 percent with the Nifty 50 closing above psychological 25,000 mark and continuing northward journey for second consecutive week. The rising hope for stronger earnings in second half of current financial year post GST rate rationalisation, and benefits of monetary easing lifted market sentiment.

Further, the market found support in improving prospects for India–US trade negotiations despite continued foreign outflows weighing on the rupee. In between, the gold futures reached fresh highs $3,715.2 per troy ounce on strong safe-haven demand amid global trade tensions, closing 0.91 percent higher for the week at $3,686.4.

In the coming week starting from September 15, the market is expected to remain positive with focus on central banks' interest rate decision (including FOMC) and further development, if any, with respect to India-US trade deal.

The Nifty 50 rallied 373 points (1.51 percent) to 25,114, and the BSE Sensex soared 1,194 points (1.48 percent) to 81,905, while the Nifty Midcap and Smallcap 100 indices performed better than benchmarks, rising 2.02 percent and 1.9 percent, respectively.

According to Siddhartha Khemka - Head of Research, Wealth Management at Motilal Oswal Financial Services, the near-term market outlook remains constructive, albeit with potential volatility around central bank events.

Progress in India–US trade negotiations could provide an additional boost to investor confidence, he said.

Among sectors, the Nifty IT index was the biggest gainer, rising over 4 percent during the passing week on hope of a Fed rate cut, Infosys’ buyback announcement, and optimism over a revival in technology spending.

Further, the Nifty Auto gained 2 percent supported by expectations of GST-driven demand recovery and festive season tailwinds. Domestic CPI inflation registered a slight uptick; however, ongoing tax reforms are expected to help ease pressures in the period ahead, Vinod Nair, Head of Research at Geojit Investments said.

Here are 10 key factors to watch next week:

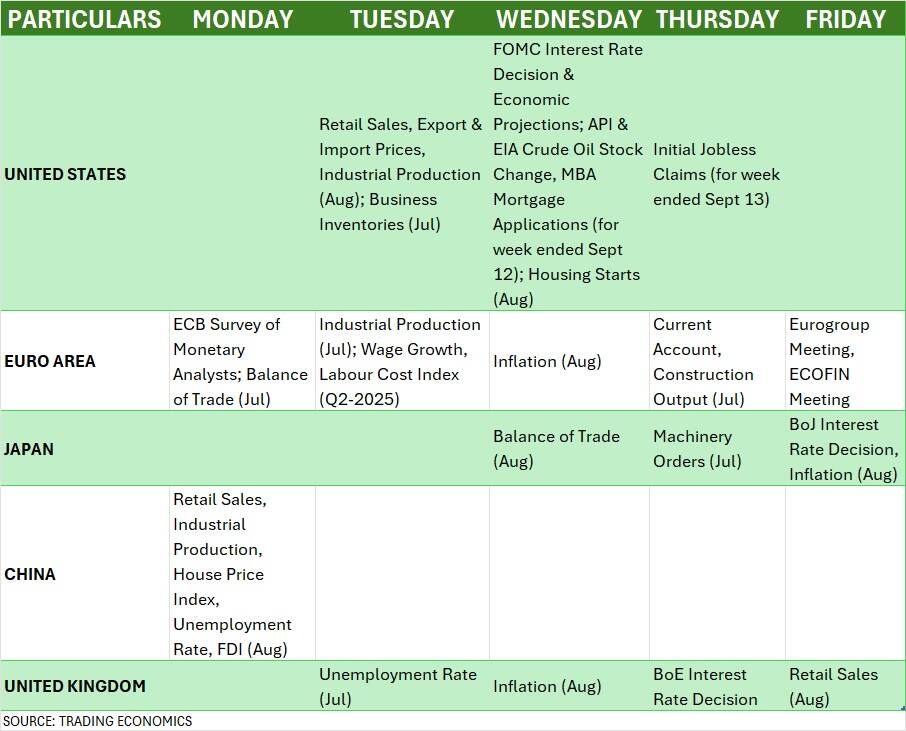

FOMC Meet

Globally, all eyes will be on the Federal Reserve's two-day meeting, concluding on September 17. Most economists expect the 25 bps cut in fed funds rate following weak jobs data, which according to them seems to have already priced in by the asset classes, but Fed Chair Jerome Powell’s commentary and its forward-looking signals regarding the Fed’s stance (given the slowdown in labour demand) along with updated economic projections for 2025 are the key to watch.

Meanwhile, President Trump has requested that a federal appeals court pause a lower court ruling that blocked his attempt to remove Fed Governor Lisa Cook over allegations of mortgage fraud. He is seeking an emergency decision by Monday, just one day before the FOMC convenes. If Trump’s Fed nominee Stephen Miran, a Treasury official, secures approval to join the Fed Board early next week, he may push for a more aggressive 50-basis-point rate cut, potentially shifting the balance within the policymaking committee, according to Kaynat Chainwala of Kotak Securities.

Apart from Fed meet, the focus will also be on the monthly retail sales, and weekly jobs data by the United States next week.

Bank of Japan, Bank of England Policy Meetings

Further, the market participants will also closely track the interest rate decisions by the Bank of England and Bank of Japan for their implications on global liquidity and risk sentiment.

According to most global economists, the Bank of England is expected to maintain its interest rates unchanged at 4 percent in its policy meeting on September 18 due to elevated inflation, though there is a possibility rate cut in December quarter.

Meanwhile, at the end of two-day meeting on September 19, the Bank of Japan is also likely to keep rates steady at 0.5 percent, but the Governor Kazuo Ueda's commentary about further interest rate decision and economic outlook amid US tariff hit will be watched.

Global Economic Data

Apart from central banks decision, economic data points by China, United Kingdom, Euro Zone and Japan will also be watched next week. Europe will release its monthly inflation, industrial production, and balance of trade, along with quarterly wage growth.

Japan and United Kingdom will also announce its inflation numbers for August next week, while the China is set to release its retail sales, industrial production, unemployment rate, and FDI numbers for August next week.

Domestic Economic Data

Back home, WPI inflation, unemployment rate, and balance of trade numbers for the month of August will be announced on September 15, while foreign exchange reserves for the week ended September 12 will also be released next week on September 19.

The market participants will also check the sentiment at the FIIs (foreign institutional Investors) desk, as the selling pressure by FIIs was less compared to several previous weeks. If they gradually turn net buyers in the Indian equities, the market sentiment which has improved in the last two week may remain strong in the coming weeks as well, as on other side, DIIs (domestic institutional investors), the strong believer in the India story, already net buyers for several quarters, combining both can give robust boost to the market, according to experts.

FIIs have net sold Rs 3,577 crore in the passing week, against Rs 5,667 crore worth of net selling in previous week. On the contrary, DIIs have net bought Rs 13,703 crore worth shares in addition Rs 13,444 crore in the same periods.

The Indian rupee continued to depreciate for third consecutive week, weakening 0.12 percent to end at all-time closing low of 88.25 after hitting an intraday life low of 88.47 against the US dollar, pressurising by the higher US trade tariffs and FPI selling pressure, though upward GDP revision after GST rate rationalization and Fed rate cut hopes supported the currency.

Manoj Kumar Jain of Prithvifinmart Commodity Research expects the rupee to remain volatile next week amid volatility in the dollar index, volatility in the domestic equity markets and FOMC meetings. "The rupee could trade in the range of 87.4000-89.5000 next week," he said.

Meanwhile, the US dollar index remained in the consolidation and below all key moving averages for several weeks now, declining 0.12 percent during the week to 97.62 after rangebound trade, amid disappointing US job data and higher-than-expected CPI inflation.

On the primary market front, investors will see total six new initial public offerings (IPOs) next week with 3 each in the mainboard and SME segments.

In the mainboard segment, Euro Pratik Sales, the marketer and seller of decorative panels and laminates, will open its Rs 451-crore IPO for subscription on September 16, followed by TMT bars maker VMS TMT's Rs 149-crore initial share sale on September 17. Bengaluru-based technology solutions provider iValue Infosolutions is the latest one in the segment, launching its maiden public issue on September 18.

SME companies like Vijay-Kedia backed TechD Cybersecurity, aluminium products maker Sampat Aluminium, and cables and wires manufacturer JD Cables will also open their IPOs next week on September 15, September 17, and September 18, respectively. Further, Airfloa Rail Technology, and LT Elevator IPOs will remain open for subscription till September 15 and 16, respectively.

On the listing front, Urban Company, Dev Accelerator, and Shringar House of Mangalsutra will make their market debut on BSE and NSE on September 17, while in the SME segment, nine new companies - Vashishtha Luxury Fashion, Krupalu Metals, Nilachal Carbo Metalicks, Karbonsteel Engineering, Taurian MPS, Jay Ambe Supermarkets, Galaxy Medicare, Airfloa Rail Technology, and LT Elevator - will be available for trading.

Technical View

Technically, the Nifty 50 is looking much better than previous week backed by technical and momentum indicators as it started trading well above all key moving averages & midline of Bollinger bands, strong bullish candle formation, and bullish crossovers in RSI, MACD with strength in histogram. Hence, if the index decisively surpasses and sustains August high (25,154) in the coming week despite likely consolidation due to consistent rising for last eighth consecutive session, the fresh leg of upmove toward 25,250, 25,550 and June high (25,669) can't be ruled out, provided the index holds 25,000 as an immediate crucial support, according to experts.

F&O Cues

The weekly options data suggested that the 25,200-25,300 is expected to be the immediate resistance followed by 25,500, with strong support at 25,000.

The maximum Call open interest was placed at the 26,000 strike, followed by the 25,500 and 25,200 strikes, with the maximum Call writing at the 25,150, 25,300 and 25,350 strikes, while the 25,000 strike holds the maximum Put open interest, followed by the 25,100 and 24,900 strikes, with the maximum Put writing at the 25,100, 25,050 and 25,150 strikes.

India VIX

The India VIX, which measures expected market volatility, hit fresh all-time closing low, signalling strong comfort for bulls and less uncertainty and volatility in the short term. The fear index dropped 6.1 percent during the week to 10.12, the lowest closing level in the history, in addition to 8.27 percent decline in previous week.

Corporate Action

Here are key corporate actions taking place in the coming week:

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.