The broader indices remained under pressure and lost between 0.6-1 percent amid volatility led by weak start of the India Inc earnings, uncertainty around trade negotiations with US, and President Donald Trump's plans to impose blanket tariffs of 15% or 20% on most trade partners.

Among broader indices, the BSE Small-Cap index shed 0.6 percent, while BSE Mid-Cap and Large-Cap indices fell 1 percent each. The mid and small-cap indices snapped 2-week gaining momentum, while large-cap index extended the fall in the second week.

For the week, the BSE Sensex index declined 932.42 points or 1.11 percent to end at 82,500.47, and Nifty50 shed 311.15 points or 1.22 percent to finish at 25,149.85.

The Foreign Institutional Investors (FIIs) extended their selling on second week, as they sold equities worth Rs 4,511.12 crore, meanwhile Domestic Institutional Investors (DII) continued their buying in 12th week as they bought equities worth Rs 8,291 crore.

On the sectoral, BSE Telecom index shed 4.4 percent, BSE Information Technology index fell more than 3 percent, BSE Consumer Durables shed 2.7 percent, BSE Metal, Energy, Auto, PSU Bank, Oil & Gas down 2 percent each. BSE FMCG index added 2 percent, while Power index rose 0.6 percent.

"The domestic indices witnessed two consecutive weeks of selling amid persistent global trade tensions and a weak start to the earnings season. Delays in finalizing the India–US trade pact, coupled with the US decision to extend tariff deadlines, have added to short-term uncertainties. Additionally, the US move to impose a 35% tariff on Canada further dampened market sentiment," said Vinod Nair, Head of Research, Geojit Investments.

"Consumption-oriented sectors such as FMCG and discretionary stocks experienced selective buying, supported by signs of urban demand revival and improving margins. A backdrop of easing inflation, declining interest rates, and a favourable monsoon contributed to the overall positive undertone."

"Broader indices slipped into negative territory due to a lack of triggers to sustain current premium valuations and uninspiring results from a key IT bellwether, which raised concerns over FY26 earnings estimates. As Q1FY26 earnings unfold, investors are closely monitoring guidance on margins and sector dynamics. Upcoming economic data releases including inflation figures from the U.S. and India, as well as China’s GDP numbers are expected to draw investor attention," he added.

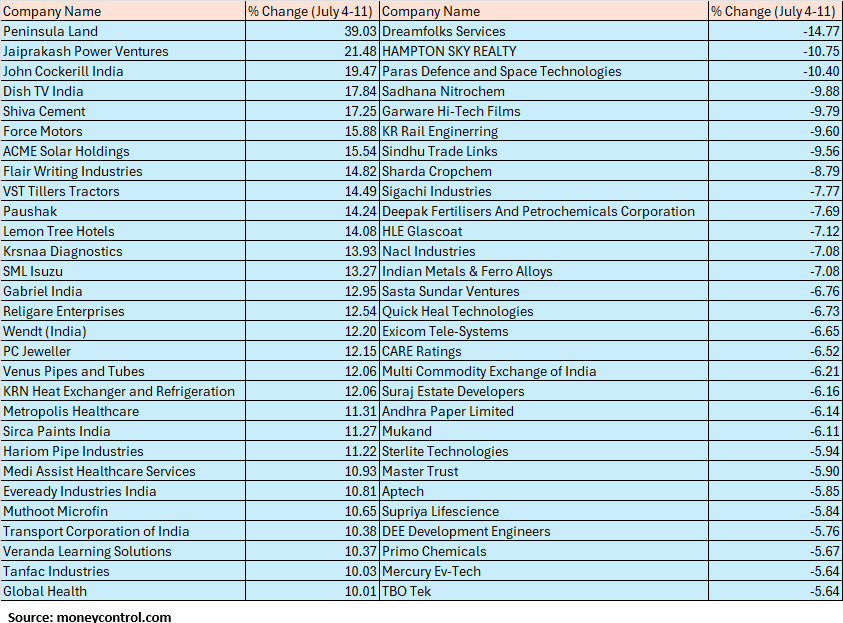

The BSE Small-cap index shed 0.6 percent with Dreamfolks Services, Hampton Sky Realty, Paras Defence and Space Technologies, Sadhana Nitrochem, Garware Hi-Tech Films, KR Rail Enginerring, Sindhu Trade Links, Sharda Cropchem, Sigachi Industries, Deepak Fertilisers And Petrochemicals Corporation, HLE Glascoat, Nacl Industries, Indian Metals & Ferro Alloys falling between 7-14 percent.

On the other hand, Peninsula Land, Jaiprakash Power Ventures, John Cockerill India, Dish TV India, Shiva Cement, Force Motors, ACME Solar Holdings gained between 15-39 percent.

Where is Nifty50 headed?

Nagaraj Shetti, Senior Technical Research Analyst at HDFC Securities

Nifty on the weekly chart slipped below the crucial support of around 25200 levels as per change in polarity. Further weakness from here could indicate a failure of the decisive upside breakout of the larger range movement as per weekly timeframe chart.

The underlying trend of Nifty has turned down. Further weakness from here could drag Nifty down to 24800-24700 levels by next week. Any pullback rally could find resistance around 25300 levels.

Amol Athawale, VP- Technical Research, Kotak Securities:

On weekly charts, Nifty has formed a bearish candle, and on daily charts, it has formed a lower top formation. Additionally, after a long time, Nifty slipped below the 20-day SMA (Simple Moving Average) zone, which supports further weakness from the current levels. We believe that as long as the market remains below 25,300/83000, the weak sentiment is likely to continue. Below this level, the market could slip to the 50-day SMA or around 25,000/82100. Further downside may also continue, potentially dragging the market down to 24,800-24650/81500-81100.

On the other hand, if the market trades above 25,300/83000, sentiment could improve. If the market manages to stay above this level, it could move up to 25,550–25,650/83700-84000.

Siddhartha Khemka, Head - Research, Wealth Management, Motilal Oswal Financial Services

As the earnings season progresses, markets are expected to witness volatility driven by stock-specific factors. Adding to the cautious tone, President Donald Trump stated that he plans to impose blanket tariffs of 15% or 20% on most trade partners.

The lingering uncertainty around trade negotiations is likely to keep markets in a consolidation mode. Investors will now focus on key domestic macro data, including CPI and WPI inflation prints, while tracking ongoing Q1 earnings and updates on the India–US trade deal.

Rupak De, Senior Technical Analyst at LKP Securities

The Nifty continues to remain weak as the index slipped below the previous swing low on the hourly chart. Additionally, it has fallen below the 21 EMA on the daily timeframe.

Momentum also remains weak in the short term, with the RSI in a negative crossover. However, after the recent decline, the index has approached the support of the 200-hourly moving average.

A move above 25,150-25,160 in the initial trading hour could trigger a rally towards 25,250 and 25,400. On the downside, support is placed at 25,090 and 24,900.

Disclaimer: The views and investment tips expressed by experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.