Ruchi Agrawal Moneycontrol Research

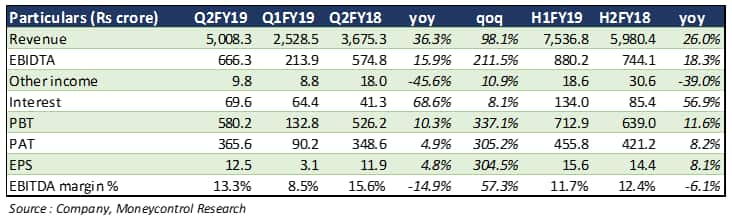

Coromandel International (CORO) reported a restrained quarter with pressure on margins from high raw material costs. The revenue for the quarter was up 36.3 percent year on year (YoY) on the back of volume rise in fertilizer business. While earnings before interest, tax, depreciation, and amortisation (EBITDA) grew 16 percent YoY, the margins saw 230 basis points YoY contraction due to increased input costs and lag in price hikes. Rupee depreciation also ate away some of the quarter’s profitability.

Fertilizer segment volumes surge

With an increase in the share of high margins fertilizers in the product mix, the fertilizer and nutrient segment saw a healthy growth. Phosphatic fertilizer business grew 28 percent YoY and sale of unique grades grew by 35 percent YoY. While MOP sales declined, urea sales saw a substantial uptick during the quarter.

The price of phos acid has been on an upswing. This has led to reduced interest in the production of DAP as more manufacturers want to divert phos acid use towards the production of high-grade NPK products where margins are higher. This has led to higher import for DAP. Moreover, with increased product prices, farmers are moving to lower grade products with low phosphate content which has increased the demand for the company’s unique grade products.

Crop Protection business

The segment saw a sales uptick of 14 percent YoY with volume growth in South America and Africa. The company launched two new products in the segment during the quarter. The company is now investing to expand the capacity of the mancozeb facility along with an expansion of production for the new products towards Q4FY19. With the acquisition of the bio pesticides business of EID Parry, CORO is now looking to expand in North America and Europe.

The drought-like situation in Rayalaseema and North Karnataka led to softness in retail sales during the quarter. Due to this, the share of non-fertilizer products segment dipped from 42 percent to 37 percent.

Outlook

Healthy reservoir levels coupled with the forecast of a normal north-east monsoon bodes well for the upcoming Rabi season. With major exposure in the southern states, we believe this would work in favour of a healthy second half for the company. Price hikes scheduled to be taken from November 1 in the NPK segment coupled with low discounts stand to ease the pressure on the margins in the current quarter. Moreover, the company has built a significant inventory of phos acid since the start of the year in anticipation of surging price, which should benefit margins in the current quarter. Low channel inventory at the start of 2HFY19 stands as a positive for volumes and pass on of price hikes.

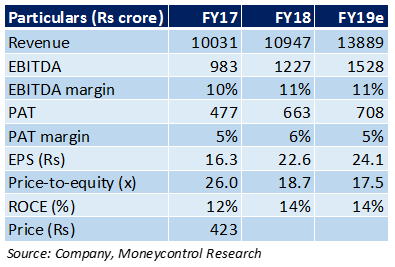

The stock has corrected in the last 6 months and is trading 28 percent below its 52-week high and at a 2019e (estimated) PE of 17.5x. Though we expect the pressure on margins to continue in the short term, we expect healthy growth in the longer run due to growing share of the non-subsidy business, greater operating leverage and visibility of growth in crop protection business. We find the business fundamentally sound and believe the pressure from external anomalies which is restraining the growth to diminish in the future.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.