Anubhav Sahu Moneycontrol research

JHS Svendgaard, reported an encouraging set of results driven by commissioning of new capacity and better sales offtake at its key clients end, Patanjali and Dabur. While we took note of company’s capacity expansion updates, it’s near-term sales guidance, in particular, adds to our conviction for the stock.

Dabur, too, posted a spectacular result, beyond oralcare. Double digit growth in most of the product categories and higher rural growth (vs. urban growth) were the key takeaways.

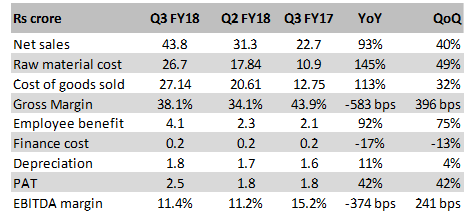

JHS Q3 2018: guided by improved volume offtake

JHS Q3 FY18 results witnessed 40% QoQ (93% YoY) growth in net sales driven by operationalization of new capacity and enhanced contracts from the clients. Gross margin improved sequentially but declined on YoY basis. EBITDA margin, as well, improved sequentially but expansion was lower due to higher employee cost and other expenses. Further, margins were also impacted by the cost related to their own brand, where in its manufacturing is likely to scale up in the current quarter.

New capacity commissioned in Q2 FY 2018

It is noteworthy that company has commissioned its toothpaste manufacturing capacity to 175 million tubes (from 90 million tubes) which is now aligned with its manufacturing cum packaging capacity of 28,000 TPA.

Management expects 25% growth in FY19

Management seems upbeat on the utilization of current capacity both in terms of order book from the clients and as well as plan to manufacture own brand products.

Currently, own brand products constitute 10% of sales which is likely to scale up from current quarter (Q4FY18). Management expects 25% growth in both topline and bottom-line for FY19.

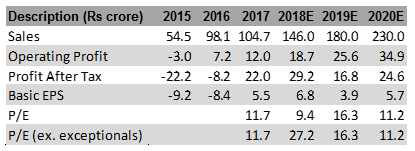

Reasonable valuation

Results have been largely in-line with our expectations prompting minor tweaks in our projections. We are encouraged by the sequential jump in the topline numbers guided by the new capacity expansion and expect incremental increase in capacity utilization.

Stock is currently trading at 16.3x (2019E earnings) which is at a discount to the industry average. Further, in light of 42% CAGR for the operating profit for the period 2017-19E, valuation appears attractive, in our view. Recent dip in stock prices provides an interesting entry opportunity for the investors.

Further, Q3 results of its key client Dabur has consistently been robust in the oral care category (Q3FY18: 26% YoY sales growth in toothpaste) which lends credence to the growth story of JHS.

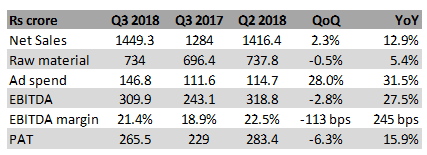

Dabur Quarterly update:

Dabur’s reported consolidated revenue for Q3FY18 increased by 6.1 percent YoY, while the underlying constant currency growth (adjusted for GST accounting) was up 12.9 percent. Indian business (74 percent of Q3 FY18 sales) was up 17.7 percent YoY mainly aided by 13 percent volume growth. International business grew by 5 percent on constant currency basis. India business EBITDA margins improved on YoY terms but contracted on QoQ terms due to pick up in ad spends partially offset by lower raw material cost.

Well diversified performance

In terms of product categories, there was double digit performance from all except OTC and Food.

In fact, growth in Food segment (14% of sales) was flat partially due to high base effect. But the main impact resulted from the shift in festival season and competition from the mid-sized value players like hector bioscience.

Health supplements (24% of sales) vertical benefitted from strong growth in Chyawanprash (+12.2% YoY) and Honey (+33.2%). Although, it’s happening on weak base, but market share gains in honey segment underlines claw back of position in the market. Home care, relatively, smaller segment witnessed good growth for Sanifresh and Odonil partially offset by weak numbers for Odomos (lower mosquito related diseases).

Oral care, particularly tooth paste category, continue to deliver. While strong growth in south continues, there has also been market share gain in states like UP, where it had earlier lost some ground.

Focus on domestic business

In the Food segment, company garners high margins and is ready to sacrifice some and meet competition on the pricing front. However, on the overall pricing front, company is in a wait and watch mode as the Oil derivative prices have surged and at some point price hikes may be warranted.

In case of international business, GCC markets have witnessed turnaround but North African, Turkey markets were weak. Consequently, ad spend in international markets have still not picked up, in contrast to the domestic market. So in near term, focus is on the domestic market recovery.

Outlook

Overall, we are encouraged with demand pick up in rural market. Sales growth through Super stockist channel, which is largely rural, was 26 percent YoY and augurs well for a company having sales contribution of about 45-50 percent from rural areas. Secondly, the company is able to gain better traction in competitive segments like oralcare and honey.

Thus, reducing competitive intensity, higher new product roll out, demand pick up and calibrated product-wise strategy, make us remain constructive on the stock (38x 2019e earnings vs. market leader HUL’s 49x 2019e earnings).

For more research articles, visit our Moneycontrol Research Page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!