Ruchi AgrawalMoneycontrol Research

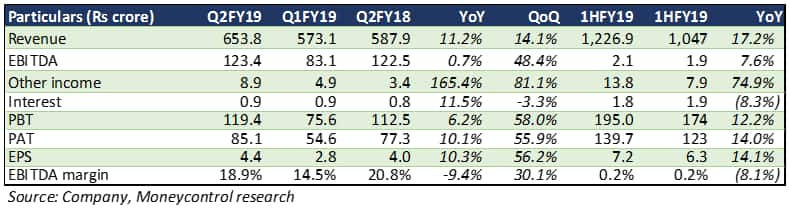

Rallis India reported a marginally improved performance on the back of traction from the international operations and price hikes, despite the overhang of high input costs. The revenue for the quarter was up 11 percent year-on-year (YoY). Owing to a 190 basis point contraction in margin, earnings before interest tax depreciation and amortisation (EBITDA) remained flat.

The decent performance in the domestic business was aided by price hikes and volumes growth in some categories. Stock up of low cost inventory towards the end of FY18 helped in maintaining the gross margins. However higher other expenses on account of higher fuel and transportation costs and some marked to market forex losses led to erosion of the EBITDA margins. The depreciation of the rupee during the quarter impacted the input cost of raw materials for the company.

The international segment of the company forms nearly one third on the business and growth in this segment remained substantially higher than the overall 20 percent growth in the business. Higher demand for herbicides boosted the growth in exports. This shows buoyancy in the LatAm and European markets.

Metahelix (seeds business), whose portfolio is majorly focused on the kharif season reported a 3 percent yoy top line growth majorly driven by strong demand in cotton and corn. However, the company continues to struggle and reported an EBITDA loss of Rs 580 crores.

Update on monsoon

This year’s monsoon, while being termed normal, remained 7 percent below the long period average with not to satisfactory temporal and special distribution and long periods of dry spells. Pest attacks were sporadic owing to dry spells, with very few cases of pink bollworm, sheath blight and other diseases in pulses. The overall cropping acreage in kharif were down 2 percent YoY. Key crops like paddy, pulses and cotton saw lower acreages with only sugarcane up 4 percent yoy.

High working capital

The company has been reporting a high working capital owing to stocking up of inventory in the 1H and higher receivable days.

The high debtor period in the last two quarters is above the companies normal and the management’s comfort. We understand from the management that compressed farm incomes has led to higher receivable days for the company. Despite a decent output in the Kharif season, most major crops are selling below MSP (minimum support price) in the wholesales markets. Compressed farmer income could lead to an impact of the purchasing power of the farmers and thereby Q3 might see some impact from this. Moreover increasing exposure to exports also contributed to this as the credit period is generally longer in international markets.

The China supply situation

The China supply situation remained an overhang and continued to have the impact on input costs for Rallis. This however is becoming the new normal and companies are now building strategies with the outlook that the Chinese supply situation would remain more or less the same. While on one hand input procurement is an issue, this is being seen as an opportunity to enter into manufacturing by many Indian firms, including Rallis.

Outlook

While on one hand good water reservoir levels bode well for the upcoming Rabi season, low liquidity in the market due to below MSP sale of the Kharif output is sucking away the purchasing power of the farmers and might have an impact on the company’s performance in 2HFY19.

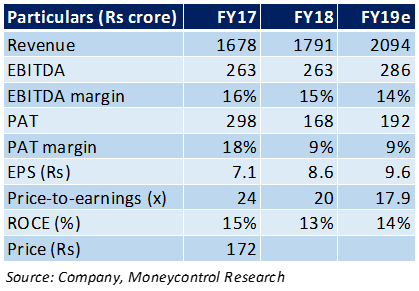

The stock has corrected almost 32 percent in the last 12 months and is currently almost 40 percent below its 52 week high post which it is trading at a 2019E P/E of 18x and an EV/EBITDA of 11x. The management is working to foray into a more profitable product mix which would augur well for the company’s margins in the longer term. Commercialisation of new molecules would be something to look out for. However, the company is currently impacted by external operating environment, and we believe the overhang would continue in the near term.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.