Anubhav Sahu

Moneycontrol research

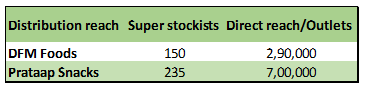

Prataap Snacks had a dream listing at the bourses last year. While valuation right from the start looked optically expensive, it may be worthwhile doing a health check in light of the recent market consolidation. The management’s focus on its core strength - pan India distribution reach, particularly in the hinterland, along with product value proposition has been instrumental in ensuring increase in market share. This along with its operational and financial strategies in containing cost, now offer conviction in earnings growth.

While the stock’s price, even after the recent consolidation, is expensive, higher earnings visibility beckons long term investor attention.

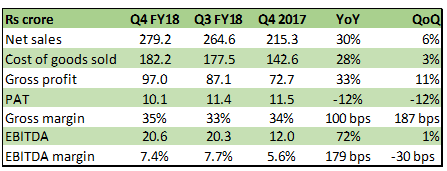

Prataap Snacks: Q4 FY18 result snapshot

Prataap Snacks maintained its sales growth momentum by posting a 30 percent year-on-year (YoY) and 6 percent quarter-on-quarter (QoQ) growth. There was a YoY gross margin improvement of 100 basis points due to better product mix, rationalisation of trade margins, change in grammage and a moderate increase in raw material cost. EBITDA margin expanded YoY as the steep increase in employee cost was offset by lower other expenses (23 percent of sales versus 25 percent of sales in Q4 FY17). Profit before tax was aided by higher other income. However, net profit declined due to higher taxes.

Prataap Snacks: Result at a glance

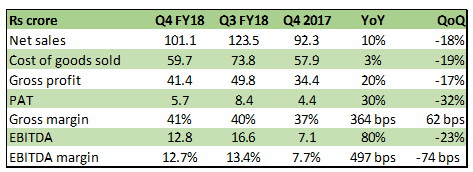

Nearest peer DFM Foods registered sequential de-growth

DFM Foods witnessed a 14 percent YoY increase in Q4 sales volume and about 360 bps improvement in EBITDA margin on the back of weak base in Q4 FY17. EBITDA margin continued to remain ahead of Prataap Snacks. On a sequential basis, the company witnessed a slowdown in sales, partially hit by failure of a specific promotion offer on its popular product category ‘Rings’. Toy offer ‘Fidget Spinner’ which was the popular promotion offer in earlier quarters, failed to evoke a similar sales response in Q4 FY18.

DFM Foods Q4 FY18 result snapshot

DFM Foods: Expansion beyond North remains a tough task

Exposure to other regions, except the north, remains a concern for DFM Foods. As most of the company’s business (about 75 percent) is limited to North India, it had been attempting to increase its reach by offering higher trade margins in the rest of the country but with limited success. It has also been increasing its reach in the north by focusing on towns with a population less than 1 lakh through a hub-and-spoke model. Competition from unorganised players remains a challenge.

In March last year, the company increased its manufacturing capacity to 26,000 tonne by brownfield expansion of 10,000 tonne in Noida. The company is working on expanding capacity of its Ghaziabad facility by 3,900 tonne by Q2 FY19. It plans a greenfield capacity expansion in Pune but the timeline is not available. With about 60 percent capacity utilisation and limited sales traction in regions other than the north, new greenfield expansion plans may be put on hold for the time being.

Comparative financials

Prataap Snacks: Expansion through contract manufacturing

In the case of Prataap Snacks, the company has expanded its reach both in terms of distribution and strategically locating manufacturing/contracting plants. Its Indore plant, which caters to most of the requirements in west, north and south India, is running near optimum capacity utilisation. Its Guwahati plant, which caters to the eastern zone only and produces non-potato chips snacks, is running sub-optimally.

Recently, the company entered into new contracts for third-party manufacturing at Ahmedabad, Bengaluru and Kolkata for producing potato chips to cater to west, east and southern regions. This might also help in reducing its logistic cost, which is currently in the range of 8-9 percent of sales, substantially ahead of the FMCG average of about 5 percent.

While it consolidates its position in the west, contract manufacturing helps in increasing market penetration in south and east. At present, the south contributes about 10 percent to overall sales.

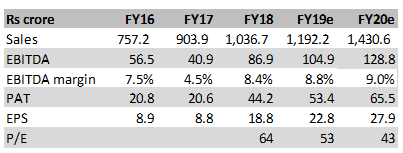

Financials and valuation

The company’s core strength has been its value positioning, along with a matching distribution strategy, wherein it targeted Tier II cities, semi-urban and rural areas. Around 75 percent of sales accrue from Rs 5 SKUs (stock keeping units). While its foray into the premium and healthy snacks category has, apparently, not been a success, increasing geographic reach and brand positioning for mass reach have been the selling points.

Over the period, key concerns - higher logistics costs and increasing geographical reach - have been partially addressed due to decentralised production through contract manufacturing.

Raw material costs, in terms of packaging (17 percent of sales), vegetable/palm oil (about 10 percent of raw material cost) and potatoes remain the key monitorables. The management has worked on a few strategies, lately, like reliance on cold storage and trading in forward contracts to contain this risk.

EBITDA margin is expected to improve gradually as it sees better demand for high margin products like Yum Pie and Nachos.

Recently, the stock has corrected 17 percent from its all-time high. It is still trading (53 times FY19e earnings) ahead of FMCG sector average by a huge margin. While we don’t expect a valuation re-rating, long term investors can consider it for accumulation on improved earnings visibility-led growth.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!