Sachin Pal Moneycontrol Research

Mahindra Logistics (MLL) and Future Supply Chain Solutions (FSCS), two of the largest third-party logistics (3PL) players in the country, reported healthy topline and operational performance in Q1 FY19.

FSCS reported year-on-year (YoY) revenue growth of 50 percent, while earnings before interest, tax, depreciation and amortisation (EBITDA) improved over 33 percent. Similarly, MLL reported 9 percent topline growth, while EBITDA surged 53 percent compared to the previous year.

The sector merits attention as growth in manufacturing and consumption demand is driving need for logistics in the country. Introduction of the Goods & Services Tax (GST) and e-way bill has further bolstered existing tailwinds in the sector and should propel the industry to double-digit growth. Investors should keep a close watch on the sector, especially 3PL players, as these companies are expected to outpace industry growth over the next few years.

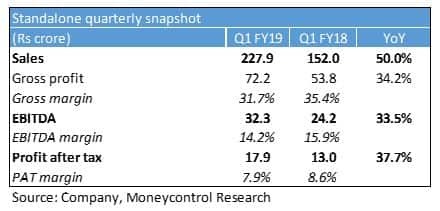

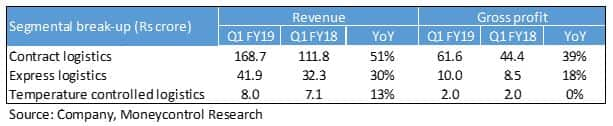

Future Supply Chain FSCS ended Q1 with a topline of Rs 228 crore, a growth of 50 percent YoY. Revenue growth was aided by strong performance of its contract logistics segment, which contributes more than 60 percent of total revenue. Revenue for contract logistics surged to Rs 169 crore, up 51 percent YoY. Other business segments - express logistics and temperature-controlled logistics - grew 30 percent and 13 percent, respectively.

Gross profit margin declined to 31.7 percent as fixed costs increased due to addition of new distribution centres as well as new warehousing space. Despite a dip in margin, growth in operating profit and profit after tax was aided by higher topline.

During the quarter gone by, FSCS added around 1 million square feet (including 0.2m sq ft from integration with Vulcan Express) of warehousing space for its contract logistics segment. The total warehousing space at the end of the quarter stood at 5.6m sq ft. The management also signed 2.62m sq ft of space for setting up nine distribution centres. Commercial operations at these facilities is expected to commence over the course of FY19 and FY20.

The company continues to diversify its revenue stream by adding non-anchor customers. During Q1, FSCS added Haldirams, Crompton Greaves and Myntra to its list of clientele. Revenue visibility looks strong, considering the sales pipeline of Rs 400-500 crore (consisting majorly of non-anchor customers), which are various stages of discussion.

FSCS’s integration with Vulcan Express, a logistics subsidiary of Snapdeal which it acquired in February for Rs 35 crore, remains well on track. During Q1, FSCS integrated six Vulcan warehouses with itself and also initiated discussions with new clients to increase utilisation of existing assets. The subsidiary reported Rs 31.7 crore in revenue and gross profit of Rs 1.5 crore in the quarter gone by. The company is in the process of rationalising Vulcan’s cost structure and aims to lower cost by 15-20 percent over the next few quarters.

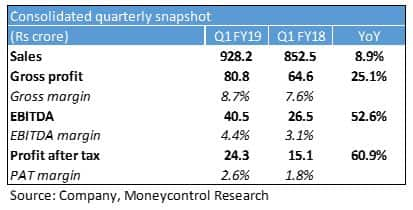

Mahindra Logistics MLL posted a Q1 revenue growth of 9 percent at Rs 928 crore. Strong performance from warehousing and other valued-added services business from the non-Mahindra vertical drove revenue growth. EBITDA jumped 53 percent to Rs 41 crore as the company benefitted from margin expansion. Operational efficiencies, along with nil strategic consulting fees (versus 3.9 crore in Q1 FY18), boosted margin profile.

Revenue from the supply-chain management grew 9 percent to Rs 838 crore. Within this segment, revenue from Mahindra group clients increased 11 percent to Rs 521 crore while the same from non-Mahindra supply chain business grew 6 percent to Rs 317 crore. Revenue from people transport solutions grew only 5 percent due to stagnation and restructuring of major customers.

Revenue growth moderated as some of its clients are still evaluating the business impact from GST implementation and are taking longer than usual to sign new contracts. Besides, it also witnessed some pricing pressure due to logistic start-ups (funded by private equity players).

The company continues to focus on warehousing and value-added services to drive revenue and expand margin. The warehousing facility in Gurugram is reaching near optimum capacity utilisation. Recently, the company leased 280,000 sq ft warehousing facility in Chakan (Pune), which is an automotive hub. The company is evaluating setting up new warehouses across locations: Delhi, Bengaluru and Chennai.

The company is increasing investments in technology to automate processes and optimise costs across divisions. It is also planning to integrate the IT systems with clients to increase customer stickiness. It plans to incur capex of Rs 20-25 crore on technology and material handling equipment in FY19.

Outlook and recommendation Industry tailwinds along with pan-India presence and strong customer relationships should help these 3PL post secular earnings growth (20-25 percent) going forward and also gain market from unorganised market players whose share currently stands around 95 percent.

FSCS has a concrete relationship with Future group companies and therefore remains well positioned to grow through strong presence in the fast growing consumption sectors, while MLL aims to leverage experience gained through its association with Mahindra group to add new business clients.

Both these companies trade at rich valuations given the high growth prospects in light of sector opportunities (GST, e-way bill and axle norms). On a one-year forward basis, FSCS trades at a price-to-earnings multiple of 28 times compared to MLL, which trades at a P/E multiple of 42 times.

FSCS is expected to grow faster than MLL (owing to its small revenue base) and trades at a significant discount to the latter. We remain confident of the growth prospects of the company and expect margin and return ratios to improve as the asset utilisation moves higher from current levels. We therefore advise long-term investors to accumulate FSCS on any correction.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!