Tech Mahindra reported a subdued performance in the March quarter, marked by weak revenue performance and softer margin. The management commentary was optimistic and the stock is inexpensive at 12.8 times FY21 estimated earnings. But given the absence of near-term currency tailwinds and the management guidance of a soft June quarter, we would wait for some more downside before turning buyers in the counter.

Key positives Overall revenue momentum slackened, but the growth in the key communication vertical (41 percent of total revenue) was strong. The management expects strong growth from this segment in future too.

The digital business grew 41 percent and constituted 31 percent of revenue for FY19. In the quarter under review, digital revenue showed a sequential growth of four percent and formed 34.1 percent of total revenue.

Strength of the BPO business was evident, with it growing 33 percent year-on-year and four percent from the previous quarter.

Also see: What should investors do with Tech Mahindra post Q4: buy, sell or hold?

Turning to verticals, in addition to the strength of the communications business, strong growth was seen in the manufacturing segment (within the enterprise business), which has now crossed $1 billion in revenue for FY19.

Deal win momentum was strong, with the company bagging deals worth $408 million in Q4. Total deal wins in FY19 were higher by 33 percent.

The company added two new clients in the $50 million bracket and four in the $20 million range. It saw three new net additions to its total clientele.

In FY19, the company saw significant (close to 290 basis points) improvement in margin to 18.2 percent. The same declined 90 bps sequentially to 18.4 percent in Q4 due to cross-currency headwinds.

Source: Company

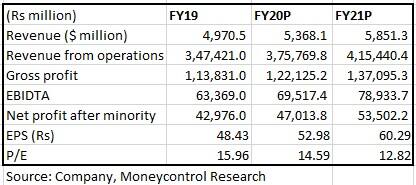

Key negatives Revenue in reported currency for Q4 FY19 stood at $1,267.5 million, a tepid YoY and sequential growth of 1.9 and 0.5 percent, respectively. For FY19, revenue at $4970.5 million showed a 4.2 percent and 5.8 percent growth in reported and constant currency terms, respectively.

Weakness in the enterprise segment, which contracted sequentially, impacted revenue. Deferral of a few projects in healthcare to FY20 and seasonal weakness in retail were the key reasons for the revenue miss.

Unlike earlier indication of a stronger growth coming from the enterprise segment, the management now expects almost similar contribution from both the enterprise and communications divisions in FY20.

In terms of geographies, the key markets of Americas and Europe (almost 77 percent share in revenue) declined, whereas the rest of the world market exhibited good growth.

The attrition rate continues to remain high at 21 percent, or the upper end of the historic band for the company. The management, however, reiterated that attrition is much less among high performers in the company.

Outlook Adoption of 5G technology is a big opportunity for Tech Mahindra and trials have commenced in markets such as the US. While the June quarter will be soft due to seasonal weakness in subsidiary Comviva, visa costs and wage hikes, the company expects gradual improvement from Q2 onwards and looks forward to a stronger second half in FY20.

The management is optimistic about the future and with contribution coming in from the communications and enterprise verticals, high single-digit revenue growth is not difficult. While the stock valuation is reasonable, we would like to wait for the currency headwind (rupee appreciation versus the dollar) to play out in the near term and would turn buyer on further weakness.

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!