Nitin Agrawal Moneycontrol Research

Highlights: - Subdued volume growth due to multiple challenges - Operating margin continues to be under pressure - Outlook for the company is weak for short-term, positive for long-term --------------------------------------------------

Eicher Motors Ltd (EML) has posted inline set of numbers amid concerns over volume growth owing to after effects of Kerala floods, and mandatory long-term insurance leading to increase in total cost of ownership.

We continue to exude confidence in the company on the back of its dominant position in bikes with engine displacement of above 250cc, outperformance of the sub-segment and positive outlook riding on customers' shift towards premium products. The valuation, however, seems to be at fair levels.

Quarter in a nutshell

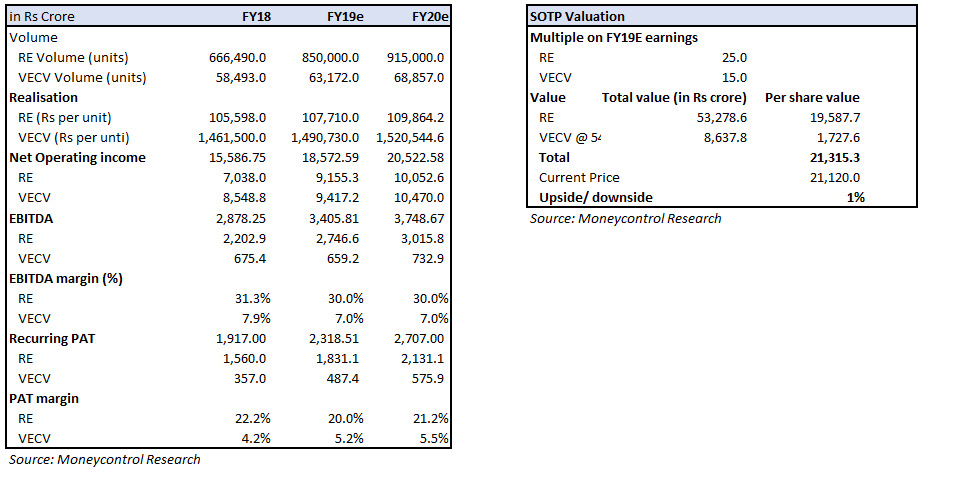

Key highlights In terms of Royal Enfield's quarterly performance, it registered volume decline of 5.9 percent on a YoY basis. The volume was hit due to overall weakness and subdued customer sentiments in auto sector led by rise in total cost of ownership due to mandatory long-term insurance, regulatory safety requirements and after effects of floods in Kerala where the demand has not yet revived. Realisation, however, witnessed a YoY increase of 10.1 percent led by price increase due to ABS (antilock braking system) implementation. Consequently, the segment posted a YoY growth of 3.6 percent in its net revenue.

EBITDA margin witnessed a contraction of 221 bps, primarily, due to expenses involved in the launch of twin bikes and continued cost pressure.

Volvo Eicher CV (VECV) witnessed 4.3 percent YoY growth in its volume and 4.3 percent YoY growth in realisation, leading to 8.8 percent growth in its net operating revenue. Its EBITDA margin witnessed a contraction of 210 bps due to higher discounting.

Outlook

Industry outlook – sluggish in near-term Two-wheeler (2W) segment has been facing challenge, primarily, due to increase in total cost of ownership driven by mandatory long-term insurance and implementation of ABS and CBS (combined braking system). The management, however, expects the situation to normalise in sometime. In light of weak demand, the management has slashed production guidance to 870-880 thousand units from 900 thousand units

Domestic market for commercial vehicle has been also facing challenges on the back of weakening macroeconomic environment leading to muted sentiments. Subdued market sentiments are on account of liquidity problem, financing issues, rising interest rates and slowdown in economic activities. This was, further, aggravated by the lag impact of new axle load norms in CV segment. We expect, demand to remain weak in the short term, but long-term growth outlook remains promising on the back of economic growth, rising income levels, lower penetration, government’s thrust on increasing rural income and focus towards infrastructure and construction.

New Launches – to grow mid-weight segment After a lull period, the company has launched two new motorcycles - the Interceptor 650 roadster and the Continental GT 650. These launches are part of its aim to lead and expand the mid-weight (250-750cc) motorcycle segment globally. The waiting period for these bikes is around 6 months and the management plans to increase the production of the same to 4,500-5,000 units by April 2019 from 2,000 units.

Continuous focus network expansion To improve penetration, Royal Enfield has been ramping up its distribution network not only in India, but also abroad. In the domestic market, the company continues to focus on distribution network and added 20 new dealers in the quarter gone by. The management expects to take the dealer count to 900 from 878 currently.

In international markets, the company added one store in Columbia, taking total stores to 8. Currently, it has 42 exclusive showrooms outside India.

Valuation: At fair level Sum of the Parts valuation suggests that the stock is currently trading at a fair valuation.

For more research articles, visit our Moneycontrol Research page.

(Moneycontrol Research analysts do not hold positions in the companies discussed here)Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!