Dear Reader,

Global financial markets traded with an eye on the developments in the Gaza Strip. Equity markets became volatile as the war raged and Israeli troops readied for a land invasion. However, with the commencement of the earnings season, increased activity was witnessed in stocks and sectors where companies announced their results.

As usual, the IT giants TCS and Infosys started the season in India. TCS missed market expectations and Infosys lowered its guidance, giving the market a slow start to the earnings season. Companies from other sectors will contribute this week and add to the market volatility.

However, the near to medium-term future of the market will depend on developments in the Middle East and oil prices.

Oil prices jumped nearly six percent on Friday, posting its highest weekly gain since February, as investors reacted to the possibility of a widening conflict in the Middle East as Israel begins ground raids inside the Gaza Strip.

Indian markets closed marginally higher for the second week after reacting negatively to the war news at the start of the week. However, the climb was slow and cautious.

Consolidation Likely

The pace suggests that participants are still weighing their options and unwilling to commit to the direction.

Adding to the caution is that next week is the penultimate week before the monthly expiry. Traders lighten their position to avoid higher margins in the final week, which can add to the volatility.

If the market rises, the exiting of positions can stall the rally. Since the move from the bottom made at 19330, the market’s rise has not been strong. Next week, markets could consolidate as every rise would be met with selling pressure. 19880 is the main hurdle for the market, which is near 61.8 percent of the September correction. We need to get past that for higher levels to be achieved.

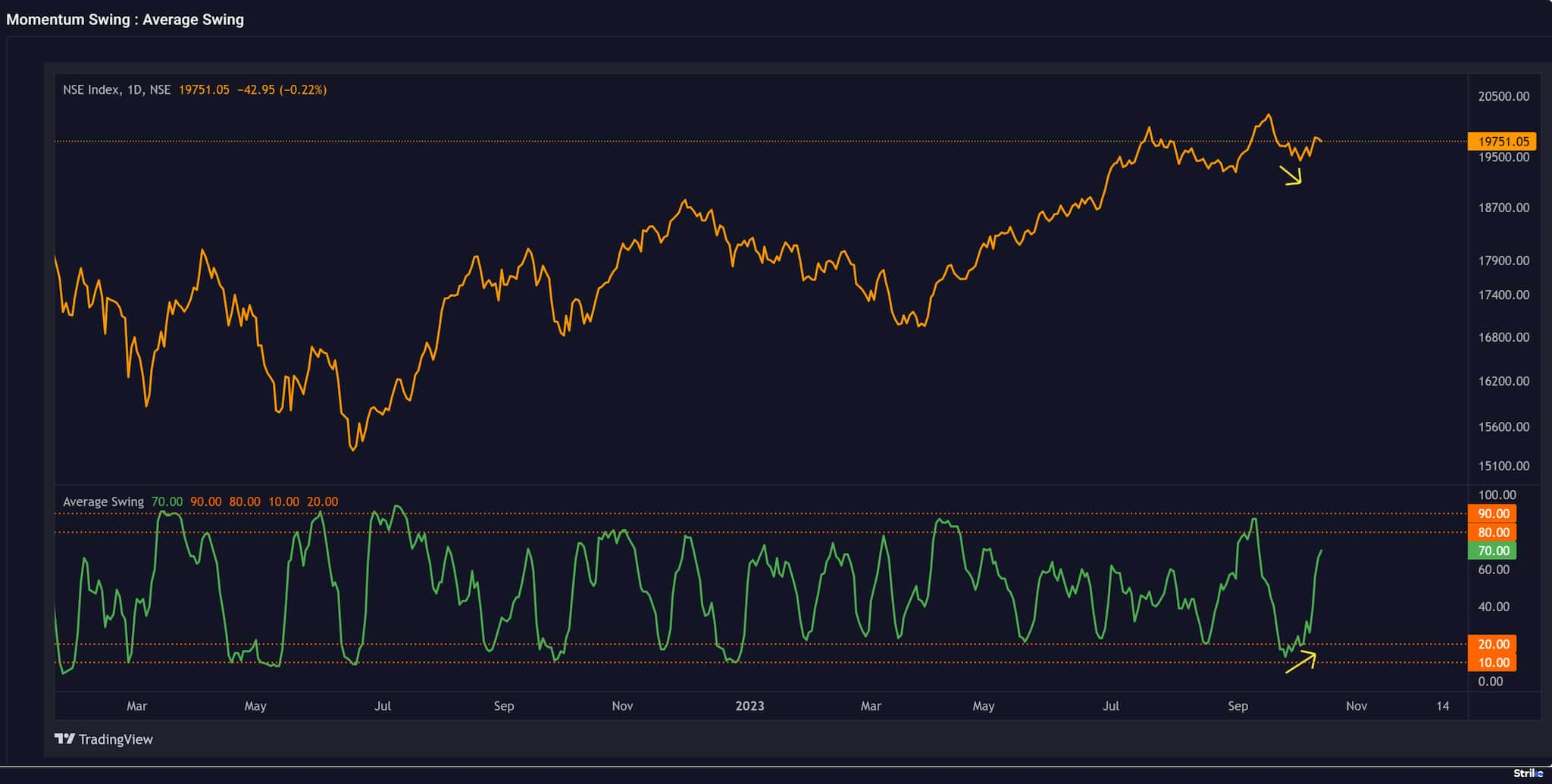

The average momentum swing continued to rise this week and is still not in the overbought zone (80) --- the current reading is 70. Chances are that just as we saw a positive divergence at the bottom, we may also see a negative divergence at the top.

Source: web.strike.money

As discussed last week, the RMI signal had fallen to four on 5th October, an extremely oversold market. Now, the indicator is gradually rising, and the reading stands at 66, indicating that more stocks are showing up on the indicator. What is lacking is the speed of the move higher.

Source: web.strike.money

Finally, FIIs remain net short on the market, though their position has reduced slightly from the peak short position of 92k contracts on 04 Oct to 81k contracts on Friday, leaving enough room for short covering. Importantly, after 17 days of selling, FIIs bought shares in the cash market, albeit in small quantities. However, they were net sellers at Rs 2199.99 crore for the week. Follow-up buying can change the market mood.

Source: web.strike.money

Indices And Market Breadth

Indian benchmark indices increased marginally during the week, with the Sensex closing 0.43 percent higher and Nifty closing 0.49 percent up.

Among the other indices, Mid-cap, Small-cap, and Large-cap indices gained 0.7 percent, 0.8 percent and 0.5 percent, respectively.

Nifty Realty continues its strong run with a 4.3 percent gain during the week, followed by the Nifty Auto index closing 2.8 percent higher. Nifty FMCG rose nearly 2 percent and Nifty Media by 1.5 percent. However, selling was witnessed in the Nifty PSU Bank index, which fell 3.2 percent and Nifty Information Technology which was lower by 1.6 percent.

ITI was the top gainer during the week with a return of 41.16 percent. Prakash Industries with 29.70 percent, and MMTC rising 26.38 percent were among the other top gainers.

Among the top losers were Lancer Containers Lines falling 13.98 percent, Themis Medicare dropping 10.24 percent and GM Breweries, losing 9.98 percent.

Global Markets

The Middle East war, high crude oil prices, dovish comments from US Fed and inflation readings kept global markets on edge.

The major global market indices ended mixed during the week.

The Dow Jones and S&P 500 closed the week higher, while Nasdaq ended the week marginally negative. Some top US banks announced the results well above market expectations, resulting in a positive closing.

During the week, some Federal Reserve policymakers made dovish remarks about the interest rate hike path. The Fed officials said there is less need to raise the Fed funds rate because of the higher yields. The September minutes of the last policy meeting confirm that the policymakers are also on the same page. As a result, the US Treasury yields declined during the week but bounced back when inflation data was released.

European markets were bullish, with the pan-European Stoxx 600 index closing higher along with Italy’s MIB and the UK’s FTSE. However, Germany’s DAX and France’s CAC ended the week lower.

Japan’s market closed higher as treasury yields declined in line with weakness in Yen.

After the Golden Week holiday, the Chinese stock markets closed in the red for the first full week of trading. Weak trade data and negative news flow on the real estate front concerning the top two developers hampered Chinese market sentiment.

Stocks To Watch

While the broad market is expected to consolidate in the coming week, certain stocks show the potential for a strong run. Among these high-momentum stocks are Bajaj Finserv, Bajaj Finance, Cholamandalam Finance, DLF, GNFC, HDFC AMC, IndusInd Bank, IPCA Labs, Lupin, and Metropolis Healthcare.

Low-risk trades that offer a good reward can be found in Asian Paints, Axis Bank and Tata Steel.

Cheers, Shishir Asthana

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.