US employers created 165,000 jobs in April, more than most analysts expected, and the unemployment rate slipped modestly to 7.5 percent, a four-year low, according to official data.

first published: Jun 7, 2013 12:47 pm

A collection of the most-viewed Moneycontrol videos.

U.S.-Iran War Intensifies; Trump Reveals Next Step, What Will Be His Next Target?

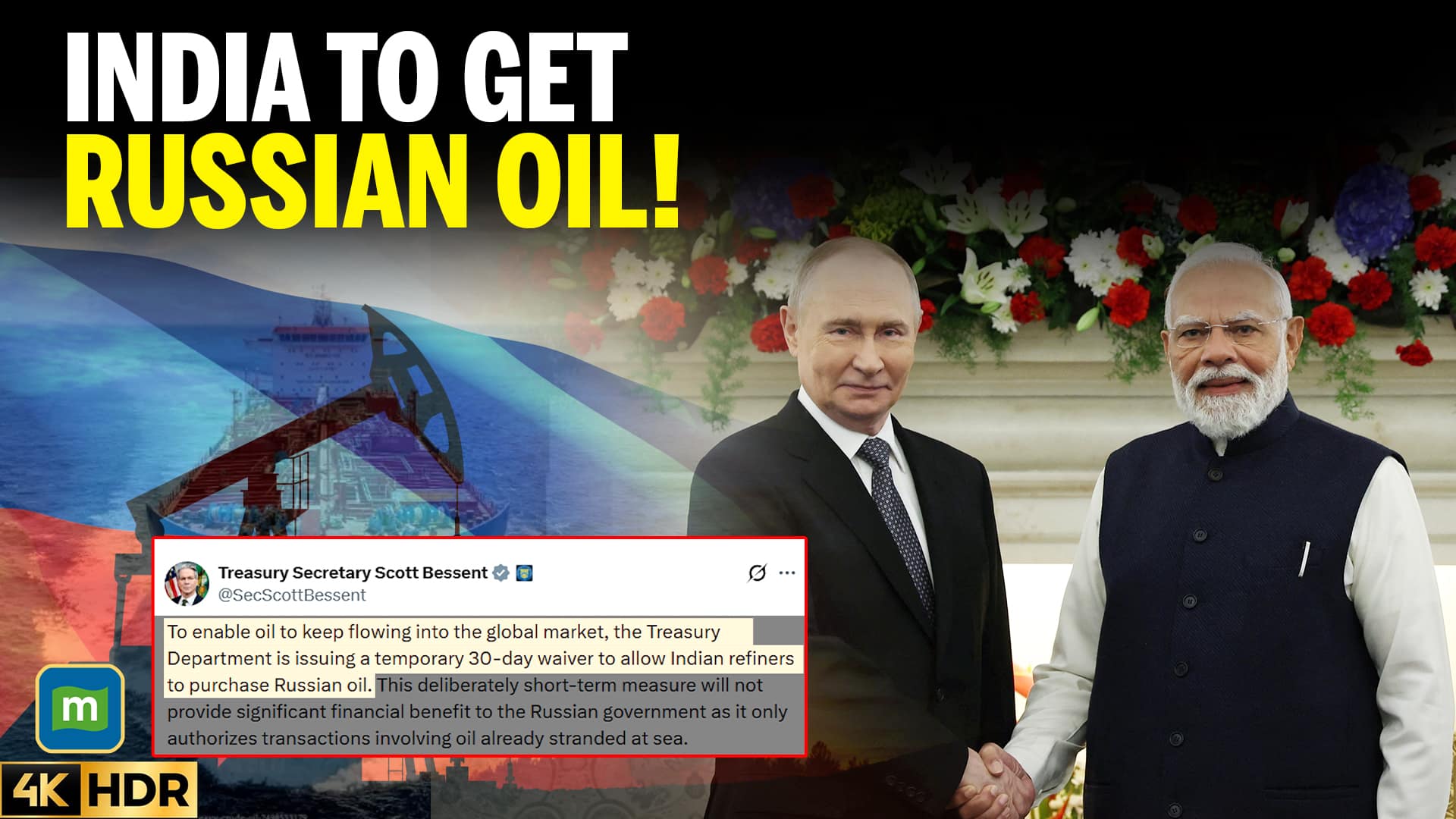

U.S. Gives India 30-Day Waiver To Purchase Russian Oil

Crude Prices Stay High; Talks To Reopen Strait of Hormuz | Trump Tariffs Under Fire | Opening Bell

Live: Nifty snaps 3-day losing streak as markets shake off war jitters | Closing Bell