Indigo Paints, the fifth largest decorative paint company in India, opens its initial public offering for subscription on January 20 with a price band at Rs 1,488-1,490 per share.

The IPO comprises fresh issue of Rs 300 crore, and an offer for sale of 58,40,000 equity shares by promoter (Hemant Jalan) and investors (Investors Sequoia Capital India Investments IV and SCI Investments V).

Many brokerage houses recommended investing in the public issue given the company's fast growth in the last decade compared to peers, expansion programme, cost-controlling measures, huge opportunity in the affordable housing segment, lowering debt and favourable growth-valuation equation.

"Despite our negative stance on the paints sector, we recommend subscribing to the Indigo Paints IPO, given the favourable growth-valuation equation," said IIFL Securities which forecasts FY20-23 sales growth at a CAGR of 20 percent, EBITDA 36 percent and PAT 48 percent versus 9 percent, 13 percent and 14 percent, respectively, for the top four peers (Asian Paints, Berger Paints, Kansai Nerolac and Akzo Nobel), on aggregate.

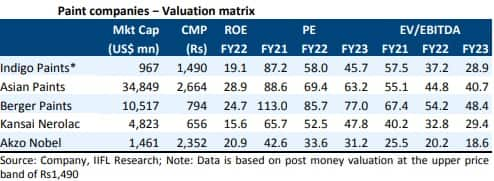

"As per our estimates, Indigo Paints would yield a valuation of 46x FY23 EPS, based on the upper price band of Rs 1,490 per share versus 63x for Asian Paints and 77x for Berger Paints. A combination of higher growth and lower valuations makes for an exciting investment opportunity," the brokerage added.

Indigo Paints IPO opens: 10 key things you should know

Indigo Paints has rapidly scaled up to become the fifth largest player in a competitive, oligopolistic decorative-paints industry in India, delivering an organic revenue CAGR of 29 percent in the past five years. Growth has been driven by differentiated products backed by heavy advertising, an incentivised workforce and a focus on smaller towns, said IIFL.

On the basis of trailing twelve months earnings, Indigo Paints is being offered at 98.5x compared to its other listed peers like Asian Paints, Berger Paints and Kansai Nerolac which are currently trading at a P/E of around 113.78x, 128.23x and 84.09x respectively, said Anand Rathi which believes that due to the lower valuations compared to its peers, Indigo Paints is placed at an attractive valuation.

Further with the planned expansion, lowering debt and other cost control measures, the brokerage is also confident that company will maintain the growth levels which is mirroring in the pricing of the IPO.

Considering these and the growth prospects in light of affordable housing push to meet PMAY (Pradhan Mantri Awas Yojna) for all by 2022 target of the Government, investors may consider an investment with a long term perspective and hence, recommended a subscribe rating to this IPO, Anand Rathi advised.

Home First Finance Company IPO to open for subscription on January 21, price band at Rs 517-518

Incorporated in 2000, Indigo Paints is the fastest growing amongst the top 5 paint companies in India, with a larger presence in Tier-III and IV towns and rural areas as well as a strong portfolio of differentiated products. It commands 2 percent market share in a highly competitive and oligopolistic decorative paints industry.

The company has three manufacturing facilities in Jodhpur, Kochi and Pudukkotai (TN) with licensed capacity of 1.02 lakh kilo litres per annum (KLPA) and average utilization of around 48 percent as on FY20. Southern and Eastern regions account for 46 percent and 29 percent of its total revenue, respectively, while rest comes from the Northern and Western markets.

It has created an extensive distribution network across 27 states and 7 union territories with 11,230 dealers / 40 depots as on first half of FY21 and installed tinting machines across their network of dealers. It intends to expand its capacities at Pudukkottai (TN) by adding 50,000 KLPA to manufacture waterbased paints to cater to the growing demand for these paints.

The company proposed to utilise the net proceeds from its fresh issue for expansion of the existing manufacturing facility at Pudukkottai, Tamil Nadu by setting-up an additional unit adjacent to the existing facility (Rs 150 crore; purchase of tinting machines and gyroshakers (Rs 50 crore); repayment certain of borrowings (Rs 25 crore); and general corporate purposes.

Indigo Paints is the 1st company to manufacture and introduce certain differentiated products in the decorative paint market in India, which includes their Metallic Emulsions, Tile Coat Emulsions, Bright Ceiling Coat Emulsions, Floor Coat Emulsions, Dirtproof & Waterproof Exterior Laminate, Exterior and Interior Acrylic Laminate, and PU Super Gloss Enamel.

To create demand for their differentiated products, Indigo Paints initially tapped into Tier 3, Tier 4 Cities, and Rural Areas, where brand penetration is easier and dealers have greater ability to influence customer purchase decisions. They subsequently leveraged this network to engage with dealers in Tier 1 and Tier 2 Cities and Metros as well.

"Indigo Paints has a track record of consistent growth in a fast growing industry with entry barriers. Company has differentiated products leading to greater brand recognition and enabling expansion into a complete range of decorative paint. Company also has leveraged brand equity and distribution network to populate tinting machines. Strategically located manufacturing facilities with proximity to raw materials helps to report better gross margins," said Keshav Lahoti (Associate Equity Analyst at Angel Broking) who is positive on the long term prospects of the industry as well the company. Hence, he recommended subscribe to the Indigo Paints IPO for long term as well as for listing gains.

Reliance Securities also recommended subscribing the issue from a long-term perspective as notably, it posted double-digit growth during lockdown in first half of FY21 and given expansion programme, increasing brand awareness, debt reduction, cost controlling measures and huge opportunity from affordable housing segment, IPL can maintain its robust growth momentum and can post superior earnings growth compared to around 14 percent and 17 percent consensus earnings CAGR of Asian Pains and Berger Paints, respectively over FY20-FY23.

Indigo Paints' revenue, EBITDA and PAT witnessed stellar 25 percent, 87 percent and 93 percent CAGR, respectively over FY18-FY20. EBITDA margin has improved from 6.5 percent in FY18 to 18.5 percent in first half of FY21 and, Reliance Securities is expected to improve further due to no exposure to industrial paints and a large salience of differentiated products.

Further, balance sheet remains healthy with D/E ratio merely at 0.13x as on first half of FY21. The company maintained the best asset turnover ratio compared to its listed peers.

"Financials have been extremely strong for this paints player with minimal debt on its books. There are a few challenges in terms of setting up a wide distribution presence amidst well established players, its skewed market presence in South India especially Kerala and rich valuations at a PE of 140x compared to sector average of 95x. Therefore, investors can subscribe to Indigo Paints for listing gains only at the moment," Nirali Shah, Senior Research Analyst at Samco Securities said.

Indigo Paints has made its brand name despite strong entry barriers due to experienced players such as Asian Paints. The company has roped in MS Dhoni as its brand ambassador and the company is actively present in the public eye due to their aggressive advertising * promotion spends accounting to around 12.7 percent of their revenue vis-à-vis peers who spend close to 4-5 percent.

"With scale and rapid growth, we expect advertising spend to grow slower than business growth, as it is already on the higher side at 12.7 percent than peers' 5.3 percent and likely lead to better margin. We believe the issue is priced attractively, and, hence, we recommend subscribe," said Elara Securities.

Disclaimer: The views and investment tips expressed by investment expert on Moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!