Ruchi Agrawal

Moneycontrol Research

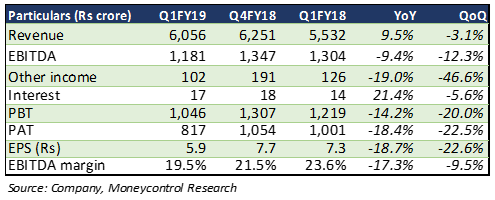

PI Industries reported a subdued Q1 with margin pressure. Revenue rose 9.5 percent year-on-year (YoY) on the back of strong volumes with a healthy pick-up in recently launched products. Growth in domestic revenue stood at 23 percent, although some benefits of a soft base quarter cannot be ruled out.

Earnings before interest, tax, depreciation and amortisation (EBITDA) saw a dip of 9.4 percent. EBITDA margin contracted 410 basis points due to firmness in raw material prices and high expenditure on marketing and research.

Switch to new accounting standards (IndAS 115) has made YoY comparison difficult. Due to the accounting change, one of the orders in the customs synthesis and manufacturing (CSM) segment, with a revenue of Rs 74 crore and profit of around Rs 21.6 crore, could not be recorded in Q4 FY18 or Q1 FY19 and has been directly transferred to retained earnings.

Results at a glance

We view the current earnings softness as a temporary phase and expect improved performance in coming quarters owing to several positive operating factors like substantial growth in the CSM segment, healthy order book line-up and favourable domestic agriculture environment.

Impact on margin Firming up of raw material prices due to strained supply from China impacted margin. PI imports around 20 percent of its raw material requirement from China. The management plans to reduce its dependence on Chinese imports and distance itself from this unstable supply with backward integration and collaborations with new suppliers in Thailand, Vietnam and Indonesia. Higher expenses on research and development and marketing and distribution of new products also ate into Q1 profits.

Domestic business Domestic business saw a healthy topline growth of 23 percent led by a strong pick up in recently launched products, healthy performance from key products like Nominee Gold and an overall positive agri environment which supported volumes. Growth is also positively impacted by a weak base due to pre-Goods & Services Tax destocking last year. The management did not offer any clarity on domestic volume growth.

CSM segment remains tangled in new accounting Offtake in the CSM segment remained subdued and reported numbers were also impacted by the change in accounting. The company has commercialised one CSM molecule during Q1 and plans to commercialise 2-3 more this fiscal. Going forward, the company has a healthy line-up of new molecules in the CSM segment along with a strong order book, which is expected to drive overall growth.

New capacity to help drive volumes PI has invested in adding new capacity, which is expected to come on-stream by FY19-end. It is also undertaking a debottlenecking process. Both these steps would help boost capacity which in turn would aid topline going forward.

Domestic agri environment to facilitate growth The domestic agri environment has been quite conducive. Implementation of the minimum support price should boost farm incomes and is expected to usher in higher volumes for crop protection products. Though acreages are down, we expect this to normalise as the monsoon progresses. Reservoir levels have been decent especially in south India where the company has major exposure. This augurs well for paddy sowing and is a positive for PI.

Outlook With a pick up in monsoon activity, healthy reservoir levels, strong product line-up and supportive policy environment, the domestic business is expected to see continued traction. Volumes are expected to improve on the back of a further pick up in recent product launches and new molecules lined-up for a launch. We expect the export situation to improve with a gradual global recovery and increased demand from international innovators.

The stock has seen a steep correction in recent months and is now trading 25 percent below its 52 week high at a FY19e price-to-earnings of 21 times. Valuation at this price point seems attractive. With a strong order book line-up and removal of current hiccups, we see the stock as an attractive pick.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!