Madhuchanda DeyMoneycontrol Research

Small finance banks had to rough it out in FY18 on twin challenges of toxic assets post-demonetisation and roll-out costs owing to conversion from micro finance lenders. They didn’t perform at the bourses despite evident signs of a revival in Q4 FY18. With macro opportunities emerging in the form of greater support to the rural economy due to generous minimum support price (MSP) hikes and prospects of a normal monsoon, the moot question is are they ripe for accumulation.

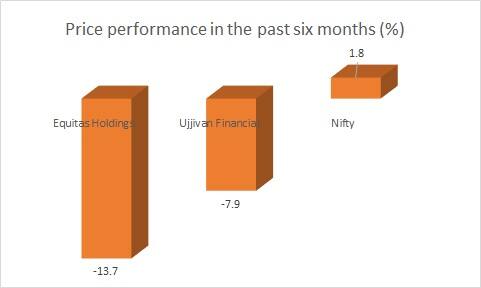

Stocks have underperformed benchmark indices

In the past six months, the stock prices of two leading small finance banks - Ujjivan Financial Services and Equitas Holdings - have underperformed the Nifty. While the yield on the 10-year benchmark bond has hardened over this period by 8.2 percent making borrowing costlier, the macro opportunities that should support the rural economy cannot be overlooked.

Source: Moneycontrol Research

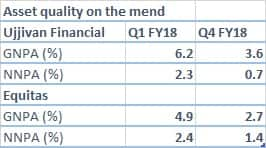

Asset quality concerns abating; bad micro finance book largely provided for

Ujjivan and Equitas have provided for/written-off their troubled micro finance book. For Ujjivan, the portfolio at risk (PAR) that touched a high of 10 percent has now fallen to 4 percent. Gross and net non-performing assets (NPA) have fallen to 3.6 percent and 0.7 percent, respectively, at the end of FY18 from a high of 6.2 percent and 2.3 percent three quarters back. Provision cover stands at 81.5 percent. Equitas too saw its gross and net NPA falling to 2.72 percent and 1.44 percent, respectively, at the end of FY18 from a high of 5.8 percent and 2.8 percent two quarters back.

Source: Company

Despite macro headwinds asset book is still growing

While FY18 was a year of challenges for both Equitas and Ujjivan, after the demonetisation-led slowdown, growth is gradually returning to normalcy. For Ujjivan, disbursement in FY18 rose 12.9 percent to Rs 8,052 crore. The company added 7.6 lakh new borrowers last fiscal. Its gross loan portfolio grew from Rs 6,379 crore to Rs 7,560 crore – an increase of 18.5 percent. In the case of Equitas, assets under management in FY18 grew 15 percent at Rs 8,238 crore.

De-risking the asset book

Both entities are moving away from a completely unsecured micro lending business model. Equitas, in particular, has come a long way and managed to pare down its micro finance book from 46 percent to 28 percent and unsecured lending from 47 percent at the end of FY17 to 33 percent at the end of FY18.

Ujjivan too is de-risking its portfolio and targeting one-third share of its portfolio from secured lending in the next 3 years. In fact, the share of micro and small enterprises (MSE) and affordable housing, which was 3 percent of the loan book at the end of FY17, improved to 7 percent at the end of FY18.

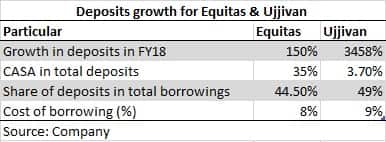

Deposit accretion to cushion margin

Diversification of the asset book in favour of secured lending comes with a risk of lower yielding assets. The only lever to protect margin is to lower cost of funds and access deposits. Thus, making it a critical differentiator.

Source: Company

Both Ujjivan and Equitas have identified it as a core focus area, although the latter so far has done a better job in garnering higher proportion of low-cost deposits. This has helped reduce its cost of deposits to 6.5 percent from 7.8 percent at the end of last year and overall cost of borrowings to 8 percent from 9.2 percent.

Ujjivan too has seen an 80 bps reduction in the cost of borrowings during the year but was reliant mostly on wholesale deposits. With a minuscule share of current accounts-savings accounts (CASA), it has enough headroom to grow its low-cost deposits base to bring down its cost of borrowings to a more competitive level.

Credit cost normalisation to propel return ratios

For Ujjivan, credit cost had shot up 400 basis points while the same for Equitas stood at 252 bps in FY18. With the toxic book of micro lending after demonetisation largely provided/written off, credit cost normalisation should propel earnings growth from FY19 onwards.

Conversion to a bank and slow business growth, marred by interest reversal, resulted in a high cost-to-income ratio for both entities. As they sweat the new infrastructure more effectively, a moderation in cost-to-income ratio should also contribute to incremental earnings.

While diversification of the asset book is likely to compress returns, the tilt in borrowings in favour of low-cost deposits should partially counter the same. Going forward, this would be one of the key matrix to monitor.

We are optimistic about credit cost normalisation to levels before demonetisation.

Valuation appears to be reasonable after the stock correction. This is especially so in the context of macro opportunities accruing from the rural economy as also inorganic attractiveness these entities would continue to enjoy, given the intrinsically profitable nature of the asset financing businesses they are engaged in.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!