Neha DaveMoneycontrol Research

Bajaj Finance, one of the largest retail asset financing NBFCs in India, posted yet another year of solid net profit growth of 46 percent year on year (YoY). The company now has an enviable track record of growing its asset book at a compounded annual growth rate (CAGR) of 42 percent and profit at CAGR 62 percent in the past 10 years.

The stellar performance reflects in Bajaj Finance's stock which has been one of the biggest wealth-creating stocks growing 67x in last 10 years (generating CAGR of 52 percent). Given the strong outperformance of the stock, should investors look at the stock incrementally, and can it continue to do well? We believe its a yes on both counts.

Earnings at a glance

Bajaj Finance - Impressive performance

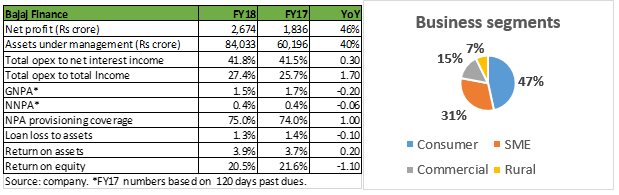

Bajaj finance posted 46 percent YoY profit growth at Rs 2,674 crore for FY18 on the back of robust loan book growth and stable asset quality. The loan book increased to Rs. 84,003 crore driven by growth in its largest business segment of consumer finance (+44 percent YoY), commercial lending (+57.0 percent YoY) while the growth in SME segment was relatively subdued at 19 percent YoY.

Growth in the SME segment dropped as the company revamped its business model and now focuses on sourcing business through cross-selling to existing customers. We view this move of shifting origination towards direct channels as prudent and expect an uptick in SME lending going forward.

The rural segment now constitutes 7 percent of the loan book, up from 1 percent in 2015 as the company has increased rural branches & franchisees to 602, which is now just tad below its urban network of 730 branches. Current rural presence is in around 10 states and the company intends to be in 16-17 states in rural business over a period of time.

The cost-to-income inched up slightly to 42 percent as the NBFC continued to expand its geographical footprint. Despite moving to more stringent regulatory asset recognition norms (from 120 days past due (dpd) in 2017 to 90 dpd in 2018), asset quality improved with gross non-performing assets and net non-performing assets at 1.48 percent and 0.38 percent, respectively, as on March 31, 2018.

While the overall operating metric continues to be superior, we are most encouraged by the new customer acquisition of 1.41 million in this quarter, growth of 48 percent YoY. Capital adequacy remained strong at 24.71 percent after raising Rs 4,500 crores through QIP in September 2017.

Bajaj Finserv – Improvement across all businesses

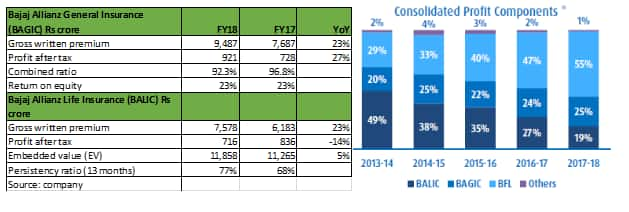

Bajaj Finserv Limited (BFS) which is the holding company for the various financial services businesses under the Bajaj group also reported healthy performance. BFS participates in the financing business through its 54.99 percent holding in Bajaj Finance and in the insurance business through its 74 percent holding in two unlisted subsidiaries, Bajaj Allianz General Insurance Company Limited (BAGIC) and Bajaj Allianz Life Insurance Company Limited (BALIC).

The key highlights of BFS’s performance were 1) significant fall in the combined ratio in the general insurance business to 92.3 percent, an improvement by 450 bps YoY and 2) continued traction in the life business with 23 percent YoY growth in gross written premium and improvement in persistency ratio across all time period (13, 25 and 37 months). Despite improving performance of insurance businesses, Bajaj Finance with 55 percent share in parent BFS’s profit, has evolved as a significant contributor to parent BFS’s profitability.

New housing finance subsidiary

To optimise the cost of funds and improve focus, Bajaj Finance has decided to move its entire mortgage business to a 100 percent housing finance subsidiary – Bajaj Housing Finance Ltd. (BHFL). The existing mortgages portfolio of Bajaj Finance will continue to run down gradually on its book while all incremental sourcing and disbursements will happen in the BHFC. The management expects to increase the share of mortgage products to ~35 percent against ~29 percent currently.

Though the margins in housing finance business are relatively low due to intense competition in the space, we view the move as desirable as mortgage business will be to provide scalability and risk reduction from a long-term perspective.

Bajaj Finance’s existing customer franchise of 26 million is estimated to have around Rs 5 to 6.5 lakh crore of outstanding mortgage loans. Bajaj’s ability to onboard them as its mortgage customers offers immense growth opportunity. Moreover, there is significant opportunity to cross-sell products.

Earnings growth sustainable

Going forward, while there is a macro headwind in the form of rising interest rates that can compress margins, the micro business of Bajaj Finance continues to be very strong. We like Bajaj Finance’s two-pronged strategy of building scale and maximising profit. Segments such as mortgages and commercial lending are focused on building scale, while consumer durable loans and personal loans are focused on maximising profit. Despite its high growth, Bajaj Finance’s loan book is only 1 percent of the outstanding credit and hence, we see an earnings growth as sustainable. The other businesses -- general and life insurance -- stand to benefit from strong sectoral tailwinds and steadily improve the performance.

Valuation is driven by “significant moat”

Consumer durable financing business requires a deep feet-on-street and a considerably evolved risk assessment processes, stringent underwriting norms, agile monitoring and superior collection mechanisms. With the usage of technology, Bajaj Finance has succeeded in creating all of these and build a superior franchise with significant moats.

Its total customer franchise strength is comparable to that of HDFC Bank. For example, Bajaj finance’s EMI (Existing Member Identification) card base of more than 12.9 million is higher than the 8.5 million outstanding credit cards of the market leader HDFC Bank as at end March 2018.

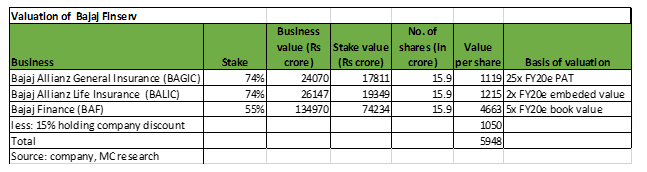

We also like the insurance franchise housed within Bajaj Finserv and see upside to Bajaj Finserv’s valuation driven mainly by the lending franchise and well supported by insurance businesses. However, given the fact that holding company structure has certain inefficiencies and awaiting clarity on Allianz’s stake in the insurance business, we prefer Bajaj Finance over Bajaj Finserv.

Bajaj Finance’s stock is currently trading at FY20e (estimated) P/B ratio (price-to-book) of 5 which is a premium to many other NBFCs. Given Bajaj Finance’s best-in-class return ratios with return on equity (RoE) at 20 percent and earnings growth above industry average, we expect premium valuations to sustain. Bajaj Finance remains the best-positioned business in the space, making it a must-own core holding amongst Indian NBFCs. Investors looking for a business with a considerable moat and high earnings growth should buy into the stock.

For more research articles, visit our Moneycontrol Research page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!