« Back to moneycontrol

SBFC Finance (SBFC; CMP: Rs 110; M Cap: Rs 12,049 crore; Rating: Overweight) has been able to consistently grow its core operating profit at a faster rate than the loan book, backed by the right asset mix, well-diversified funding base, and strong on-ground execution.

The healthy stock performance year-to-date (YTD) mirrors the company’s higher growth and strong return ratios.

Will the valuation premium sustain amid rising competitive intensity?

Increasing scale of operation

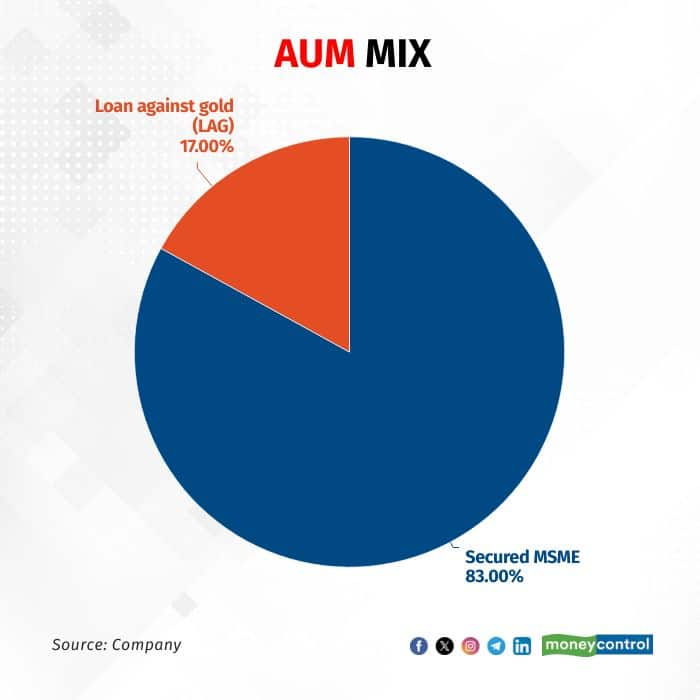

SBFC Finance offers loans against property (LAP) and gold loans to MSME (micro, small and medium enterprises) customers in the informal segment.

The distinct business mix has helped the company to maintain steady growth amid persistent regulatory headwinds. The AUM (asset under management) is growing at a four-year CAGR of over 40 percent, albeit on a small base. The loan book has crossed the Rs 10,000-crore-mark – a key milestone.

As the company scales up its business operation, the recent re-calibration of growth strategy is a step in the right direction. SBFC has filtered out customers with multiple loans, particularly in Karnataka (over 10 percent AUM mix), which led to a 6 percent QoQ dip in disbursement volumes in the September quarter.

Despite persistent stress in one of the key geographies, AUM growth moderated slightly in Q2. Hence, the company re-iterated its growth outlook for FY26.

SBFC will add gold loans to around 15 new branches in H2FY26. Incremental branch addition and rising contribution of the high-yield gold loan mix will drive sequential AUM growth -- guided in the 5-7 percent range.

Moreover, SBFC’s pivot to higher ticket size loans, particularly in the co-origination segment (19 percent AUM mix), will contribute to growth in the medium term.

The target AUM growth in the 25-30 percent range will be driven by the significant under-penetration in the core MSME LAP (loan against property) segment on a sustainable basis.

Asset quality to stabilise, credit cost to peak out

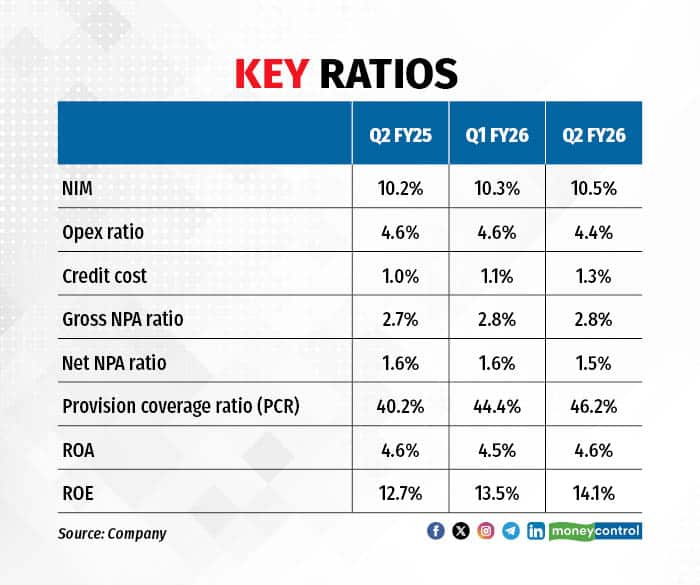

Headline asset quality numbers remained largely stable. However, a sharp uptick was seen in the early bucket delinquencies, primarily due to the seasoning of the MSME LAP book.

This led to a YoY rise of 25 basis points in the credit cost in H1, followed by an upward revision in the credit cost guidance in the 1.2-1.3 percent range.

Profitability to improve

The improvement in NIMs (net interest margins) is expected to continue on account of a better product mix, potential cost benefits, and a favourable asset-liability mix.

SBFC’s net profit crossed the Rs 200-crore-mark in H1, backed by sustained growth, stable spreads, and improved productivity. While the spread is guided to remain steady in the 9 percent range, the opex-to-AUM ratio is expected to improve, despite sustained investment in growth.

Seasoning of the MSME LAP segment could see an uptick in the credit cost. However, a better product mix will support margins and drive the RoA (return on asset).

Outlook and valuation

SBFC will leverage its strong execution capabilities to grow the loan book at a faster rate, backed by sector tailwinds in the MSME space, and cost benefits.

While the company pursues aggressive growth, it will maintain a cautious stance on asset quality. Given the continued strain in the MSME mortgage segment, the credit cost ratio is expected to increase by another 10-15 bps in the coming period, before the ratio peaks out. However, a secured loan book, tightening of credit norms, and an increase in the provision coverage ratio will likely keep the credit cost in check.

The stock is trading at a relatively rich valuation of 2.4 times FY28e book value. The valuation is justified, backed by robust growth prospects and strong return ratios.

The stock is suitable for investors with a high risk appetite, given the concentration of the loan portfolio to the vulnerable asset class.

Long-term investors can add the stock on dips.

For more research articles, visit our Moneycontrol Research page

Stay ahead. Stay profitable. Track the Key Performance Indicators of your business through various Utility Tools here. Get smart analysis on the go!!!