Preeti Kulkarni & Khyati Dharamsi

The Central Board of Direct Taxes on April 13 issued a circular detailing the process that employers have to follow this year while deducting tax from April onwards.

The clarification assumes importance as the Union Budget earlier this year introduced a new personal tax regime in which income tax rates will be significantly less for those who forego deductions and exemptions.

This is the time of the year when employers ask their employees to submit proposed investment declarations, indicate the tax deductions and exemptions that employees wish to claim during the financial year to be able to compute their taxable annual income. Mainly, the annual declaration helps employers deduct tax deducted at source every month.

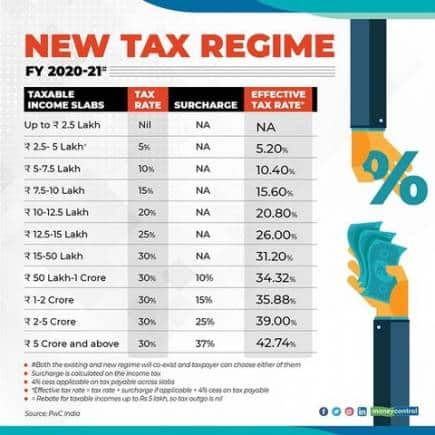

The process will be different for the financial year 2020-21 (the assessment year 2021-22). Under this optional regime, the tax slabs are liberalised and tax rates lower than the current regime (see graphic). On the flipside, you will have to let go of a host of deductions and exemptions available under the existing regime.

Since individuals have been giving a choice to select either of the two regimes by the time they file their tax return (after the entire financial year is over), employers were in a fix. That's because employers start deducting tax at source from the month of April onwards; that is the start of the financial year. Hence, the tax department has now nudged employers to start this process, rightaway; to ask their employees to choose the old or new tax regime in the month of April, itself. Communication is critical if you intend to move to the new regime. If you do not explicitly express you wish to switch to the new regime, the existing regime will be the default option.

That brings up a number of questions. Here we tackle some of them:

How will the introduction of the new tax regime change my annual proposed investment declaration filing exercise?

At the beginning of the financial year, employers ask for proposed investment declarations from their employees. They have to indicate the deductions and exemptions they intend to claim under Section 80C, Section 80D, Section 24, Section 10, etc. Under the new regime, these tax benefits will not be available.

To start with, according to the CBDT circular, you need to make a choice between the two and communicate the same to your employers. Accordingly, your employer will estimate your tax outgo for the financial year and deduct taxes while crediting your salary.

If you intend to stick to the existing regime this financial year, too, you need to share details of exemptions and deductions you plan to claim. The annual drill will remain largely the same for you.

If you wish to switch to the new regime, you will need to inform your employer. Typically, employers send out investment declaration forms in April, where you will have to indicate your choice for this year. While the paperwork under the new regime could be simpler as fewer details will need to be disclosed, remember, certain tax concessions will continue to be available in 2020-21 too. For example, employer’s contribution to National Pension System (NPS) under section 80CCD (2) and standard deduction on income from house property under section 24.

Will my employer allow me to change my choice at the end of financial year?

No. Once you take your pick, employer will not permit any changes at the time of making final investment declaration in January or February.

"Now, it is clear that the employee (only those not having income from business or profession) cannot change the option once exercised for the purposing of getting TDS deducted but can always change it at the time of filing the tax return," said Amit Maheshwari, Partner, AKM Global, a chartered accountancy firm. So far, there was no clarity on this aspect, resulting in anxiety in the minds of employers.

Does that mean I will not be allowed to change my mind later?

You can, but not through your employer. You can exercise your choice at the time of filing your returns by July 31, 2021. “You will, however, have to be careful if you wish to move back from the new regime to the existing one. This is because certain exemptions like leave travel allowance (LTA) can only be claimed through the employer and not at the time of filing return,” points out Archit Gupta, Founder and CEO, ClearTax.

So, when is the best to make this choice between old and new tax regime?

The best time is the beginning of the year. However, ensure that you do your homework well. If you are already claiming deductions, like provident fund contribution under Section 80C, you could better off in the existing regime.

Also Read | Budget 2020: Should you switch to the new income tax slabs?

As per SBI Research's estimates, less than 10 percent of the total taxpayers are expected to migrate in new tax regime as they are the only ones who will be benefited.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.