The fact that bonds come with risk, perhaps lower than equities but even so, is now dawning upon us. At least the actions of some of the investors in Non-Convertible Debentures (NCD) of some Non-Banking Finance Companies (NBFC) indicate so.

Some of these NCDs are quoting at discount to their issue price in the secondary market. For example, Dewan Housing Finance NCD offering 9.25 percent rate of interest till maturity in September 2023 quotes at Rs 715 as against the issue price of Rs 1000. Though some experts reckon this as over-reaction by investors but what are the lessons for the investors?

The problems with NBFC bond instruments have been around for the last few months. The asset liability mismatch is the chief culprit behind this. NBFCs have raised short-term money by way of commercial papers and short-term loans from banks to lend for long-term, which includes home loans. Once the short-term funding stops, the NBFCs are squeezed.

On the one hand, they have to repay the short-term loans and commercial papers and on the other, their customers pay as per the repayment schedule over an extended period of time.

To worsen the situation, the market forces tighten the liquidity situation. Either these NBFCs do not get fresh money or they get it at a significantly higher price, i.e., higher interest rates. Since these NBFCs can’t reprice their already given loans beyond a point but see their cost of funds going up, their profitability is expected to go for a toss if this continues for long period of time, which further shoo away investors.

While the future is uncertain, some of the existing investors are trying to escape by selling their NCDs at whatever price they get. “Some retail investors are overreacting to the issues faced by NBFCs and exiting the NCDs at whatever price they get on the exchange. There are asset liability mismatch and other problems. But investors should not panic,” says Ajay Manglunia, Head of Fixed Income, Edelweiss Financial Services. “It is time to stay put and let clarity emerge.”

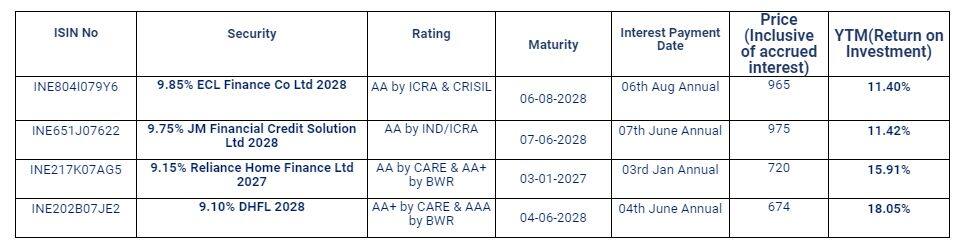

He points out that yields in the retail markets are quoting at a far higher level than the yield quoting at the institutional level in case of some bonds. This speaks for overreaction by retail investors. DHFL NCDs are quoting at 17 percent yield on the exchanges but after the news of crisis hit the markets, DHFL managed to raise money at 10 percent to 10.25 percent. Also, the asset sale has happened at yields closer to this level. Here are some examples of bonds quoting at high yield in the secondary market:

Source: Synergee Capital. Note: This is neither an exhaustive list of bonds nor are investment recommendations.

Source: Synergee Capital. Note: This is neither an exhaustive list of bonds nor are investment recommendations.

The uncertain environment has led investors to two questions – what should they be doing with their existing investments in these NCDs and what should be the learnings from these investments?

Most fixed income experts say that you do not have many choices if you are an existing investor in these bonds. “The yields at which some of these bonds quote at the moment are absurd. Nothing can be done. Just hold on to the investments,” says Joydeep Sen, Founder of Mumbai-based wealth management firm wiseinvestor.in.

If you sell now, you book losses as you sell at a steep discount to the issue price. There are companies such as DHFL where the promoters have been honouring all their repayments so far and if they manage to raise funds the way they were doing in the past, there is a fair chance that the existing investors in NCDs will be paid, he points out.

In a note that Axis Asset Management circulated among its distributors and advisors dated 31 January on its own investments in DHFL, it said that “despite the liquidity crunch, after September 21, 2018, the company has repaid loans of Rs 17,876 crore, primarily funding the same through portfolio sell-down.”

Papers across issuers may see different outcomes as the situation unfolds further. Though existing investors can’t do much, there are a few lessons for investors in future.

Investors have woken up to a harsh reality in the last six months. The safe haven called fixed income investing has emerged as a minefield. “Investors have looked at debt as a low-risk investment option. But they must understand the risk involved when they look for 2 to 3 percentage points more on bonds as compared to risk-free bonds. If you do not understand the business risk, do not venture out for higher yields,” says Ajay Manglunia.

Many investors are comfortable with a 10 percent or 20 percent fall in the prices of the shares they hold. The price erosion is a part of equity investing for them. But the same investors find it difficult to digest even 5 percent fall in the bond prices.

Fixed income instruments may aim to give you regular income, but not all come at a negligible risk like a fixed deposit. One fixed-income instrument could be riskier than the other. The problem compounds when AAA rated or AA rated instruments delays or defaults on their interest payment commitments.

“Investors must do their homework before investing. You can’t rely on the credit rating issued by credit rating agencies. If you do not understand the business and cannot arrive at an informed decision then just stay out,” says Vinod Jain, Founder and Chief Financial Planner of Jain Investment Planners. Jain says that the time has come for a change in the ways rating agencies give credit rating to investors; make investors pay for credit rating than the extant arrangement of issuer paying for credit rating.

Investors who understand the credit markets or have access to expert advice may actually end up taking informed decision going forward. However, most of the retail investors who lack the time and expertise to analyse the bond offering would find it difficult to invest going forward. In such circumstances, the investors would be better off investing in a diversified basket.

“Since most small investors lack the skillset or lack the time to analyse, it is better to invest in minimum 10 names. More the better. No single issuer should get more than 10 percent of the investible sum,” says Joydeep Sen.

“Retail investors should invest in the top notch names such as HDFC, LIC Housing Finance or the bonds issued by central government undertakings since there is a little credit risk,” says Vikram Dalal, Founder and Managing Director of Synergee Capital Services.

Investors from low income tax slabs can look for opportunities in fixed deposits. There are some opportunities to earn some extra money without taking much risk. For example, HDFC Limited (the housing finance company) offers 8.19 percent returns for a deposit maturing in 33 months, whereas HDFC Bank offers 7.4 percent for a fixed deposit of three years term.

Similar is the case if you are looking for government backed investments. State Bank of India five year fixed deposit offers 6.85 percent rate of interest whereas India Post offers 8 percent rate of interest on National Saving Certificate maturing in five years.

If you are an investor in a high income tax bracket, experts advise investing in mutual fund schemes that do not take much credit risk, banking and PSU bond funds, overnight funds or to run diversified portfolios.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.