The Monetary Policy Committee (MPC) of Reserve Bank of India (RBI) raised policy rates by 25 basis point, the first back-to-back hike since October 2013. This increase in repo rates will increase the bank’s cost of funds, which might force them to hike their MCLR.

Naveen Kukreja, CEO and Co-founder, Paisabazaar.com said: “Home loans will become costlier for fresh borrowers as and when the banks raise their respective MCLRs.”

Now, the repo-rate stands at 6.5 percent from 6.25 percent earlier. Dheeraj Singh, Head of Investments & Fund Manager – Fixed Income, Taurus Mutual Fund said, “The decision to hike rates has, quite clearly, been driven by the persistent increase in headline and core inflation that we have witnessed in the last couple of months. The likely impact of recent hikes in the minimum support price (MSP) of agricultural products on inflation has, probably, also influenced the committee’s decision to pro-actively hike interest rates.” The RBI continues to maintain a neutral stance on policy rates.

Impact on loans & advice to loan customers

Adhil Shetty, CEO, BankBazaar.com said: “In June, several leading banks including SBI had increased their MCLR. With the rate hike today, we’ll see loans get costlier.”

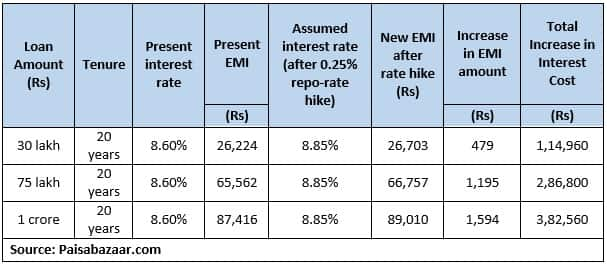

For example, on a loan of Rs. 1 lakh for 20 years at an interest rate of 8.5%, the EMI is Rs. 868. If the rate rises to 8.75%, the EMI increases to 884. If the interest rate reaches 9%, the EMI becomes Rs. 900.

“In a rising rate scenario, it makes immense sense for customers repaying loans to make periodic principal pre-payments. This is especially helpful while you’re in the first half of your loan tenure. Pre-payments made in the first half have immense impact in reducing your long-term interest outgo and thus ensuring savings,” Shetty said.

“MCLR hikes, however, will not immediately impact most existing home loan borrowers as they will continue to pay their existing lending rates till the next reset date of their loan. Once their home loan rates increase after reset date, they should first compare the new rate with those charged by the other lenders and find out the potential savings in interest cost on transferring the loan to another lender,” Kukreja said.

If the savings is substantial, borrowers should try and negotiate with their existing lenders for lower interest rates. If their existing lenders refuse to do so, they can opt for a home loan balance transfer.

Increase in EMI and total interest cost after an assumed interest rate hike of 0.25% (post repo rate hike of 0.25%)

Impact on Debt Funds

Rising rates are bad news for investors in debt mutual funds. This is because the prices of bonds fall, and bring down the NAV of bond funds. Shetty said, “It would be advisable for investors to steer clear of long-term debt funds and go for funds with shorter maturity periods. Short-term debt funds are expected to deliver lower volatility and low risk in this scenario.”

Impact on Bank Fixed Deposits

With an increase in policy rates, bank deposit rates are expected to rise as well. Just couple of days back, the SBI hiked its deposit rates by 5 to 10 bps. This means marginally higher interest earnings for customers opening fixed deposits with banks.

Impact on Small Savings SchemeWith two consecutive hikes in the repo rate, taking it to 6.50%, there is now heavy expectation of increase in small savings returns. For the April to June quarter, the rates remained unchanged. Investors looking for risk-free, guaranteed returns may continue to invest in PPF, NSC, Sukanya Samriddhi, Post Office Savings, etc.

Impact on 10 year G-sec yield

The maintenance of the neutral stance cooled bond yields after the policy announcement, as the rate hike itself was already priced in. Naresh Takkar, MD & Group CEO, ICRA Ltd, said, “Looking ahead, we expect the 10 year G-sec yield to trade in a range of 7.65%-8.0% in the remainder of this quarter. Greater clarity on MSPs, crude oil prices and other inflationary trends, fiscal risks and the central and state government borrowing programme for H2 FY2019, may emerge as triggers for a rise in bond yields. On the other hand, the announcements of additional open market operations by the RBI could help cap the G-sec yields.”

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.