Madhuchanda Dey

Moneycontrol Research

Highlights:

- Axis Bank has the potential to take over the baton from HDFC Bank

- The bank has best in class liability profile

- It is diversifying and de-risking asset book

- The new management has eyes set at 18 percent RoE

- The focus on risk-adjusted return to ensure quality

- Valuation gap with HDFC Bank to narrow

-------------------------------------------------

The worst is over for Axis Bank (CMP: Rs 732, Market Cap: Rs 188,247 crore) and it could well become the next HDFC Bank for the stock market.

In the past twenty years, HDFC Bank has demonstrated an impeccable track record of execution and the brand is now synonymous with consistency. In this period, its profit grew at a compounded annual growth rate (CAGR) of 32.5 percent, and market capitalisation at a CAGR of 34 percent.

Axis Bank, like most of its peers, could not escape the non-performing asset mess. But the crisis has forced a change of guard – which is a game changer in our view - as well as a rapid clean-up of its balance sheet. That will allow it to embark on a growth journey with quality.

Worst of the NPA cycle largely behind

Like most Indian lenders, Axis Bank witnessed a sharp deterioration in its asset quality. Its gross and net NPA that was hovering around 1.67 percent and 0.7 percent respectively in March 2016 shot up to 6.77 percent and 3.4 percent respectively by March 2018 driven largely by corporate slippages. The bank also reported a divergence with the RBI audit on recognising bad assets for FY17.

However, the clean-up led to recognition of the bulk of the stress (low-rated corporate portfolio down from Rs 27,411 crore in Q1 FY17 to Rs 7645 crore now). While higher provisioning did result in elevated credit costs, it also led to an improvement in the provision coverage ratio to 75 percent, one of the best in the industry. Going forward, with the rating downgrades largely behind, we expect normalisation of slippages as well as credit cost. That should greatly support incremental earnings.

Best in class liability franchise

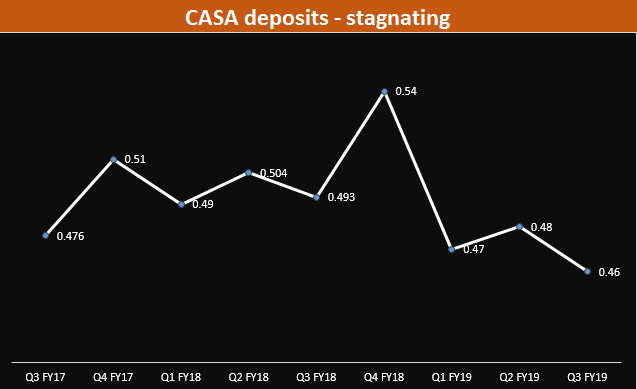

Over the years, Axis has leveraged its “branch banking model” to build a robust liability profile. The share of granular deposits is high with low-cost CASA (current and savings account) and retail term deposits close to 80 percent of total deposits.

While CASA deposits have stagnated in recent times and remains an area of focus for the new management, the bank, nevertheless, has done a commendable job on the liability side. Its market share in the banking system’s deposits has risen from 3.7 percent in March 2016 to 4.3 percent in December 2018; its incremental market share in the system’s deposits in the past one year was a high 9.7 percent. Incidentally, in the current environment, where deposit growth is lagging credit growth, Axis Bank stands out with a respectable credit to deposit ratio of 92 percent.

Source: Company

Source: Company

Diversifying and de-risking the lending book

The composition of the loan book is changing. The share of retail loans that stood at 27.4 percent in March 2013 rose to 49 percent in December 2018. Retail and SME together constitute 62 percent of the portfolio now. The bank has been broad-basing its retail offering with the addition of high-yielding products like personal loans, loans against property, credit cards etc. while trying to minimize risks by cross-selling to existing deposit customers, sourcing customers through branches and using analytics for underwriting.

De-risking efforts have gathered pace in non-retail as well, with 86 percent of the SME exposure rated at least SME3 and 82 percent of corporate exposure rated A or better. The corporate banking book is tilting in favour of working capital. The fall in the ratio of risk-weighted assets to total assets stands testimony to the gradual de-risking of the book.

With the competitive scenario weakening, in view of the stress in PSU banks and funding constraints of NBFCs, Axis Bank with its superior funding costs is in a vantage position to expand its loan book (both in corporate as well as retail) without on-boarding excessive risk and maintain an upwards trajectory in its interest margin.

Fee income: Room to improve

Fee composition is showing stability with 79 percent coming from retail and transaction banking. However, the ratio of core fees to assets at 1.1 percent suggests that there is enough headroom for improvement.

The new management could be the game changer

Axis Bank has recently seen a change of guard with Amitabh Chaudhry (ex-Managing Director and CEO of HDFC Standard Life Insurance) taking over from Shikha Sharma from January 1. We see this as a potential re-rating trigger for the bank should his articulated strategy pans out.

While growth, profitability and sustainability are the cornerstone of this strategy, what appears to be reassuring and has a striking resemblance with the HDFC group’s ethos is the focus on risk adjusted return on capital (RaRoc). The appointment of Deepak Maheshwari (formerly Group Head of Corporate Credit Risk at HDFC Bank) as the Chief Credit Officer is the first step in overhauling the underwriting processes of the bank. Several other senior management changes are being effected as well to implement the stated strategy.

Extensive use of technology, effective sweating of assets, focus on CASA (current account-savings account) and fee income and reduction in credit costs below historical average are some of the other key areas of focus with the objective of improving profitability on a sustainable basis and reaching a return on equity (RoE) of 18 percent in the next three years (by FY22).

Subsidiaries: Untapped potential

A meaningful scale up of subsidiaries is also an area of attention. So far Axis Bank’s share price does not factor in any contribution from subsidiaries and this remains a probable upside. For Axis Bank, the acquisition of FreeCharge remains a potent tool to capture digitally savvy customers. The bank plans to scale up capital market-linked businesses like Axis AMC, Axis Securities and Axis Capital, organically as well as inorganically. Axis Finance, the non-banking finance subsidiary, also has strong growth plans ahead. Finally, with an ex-insurance chief at the helm, the possibility of Axis Bank getting into manufacturing of insurance (from the present distribution only model) cannot be ruled out.

Valuation discount to HDFC Bank could narrow

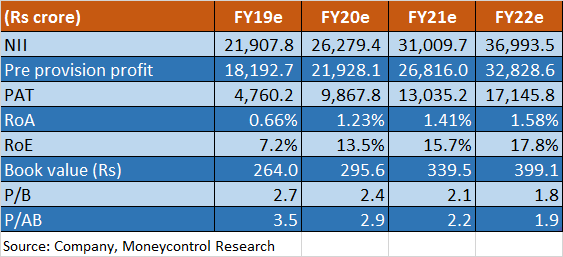

The bank had last raised capital (Rs 11,626 crore) in 2017 and has adequate resources (Capital Adequacy Ratio 16.4 percent with CET 1 11.77 percent) for growth. While there are several weak spots that warrant immediate attention, should the management succeed in addressing majority of them, the earnings traction and re-rating could be meaningful. Despite the 32 percent rally in the stock in the past one year, shares are valued at 2.1 times FY21 estimated book, a discount to HDFC Bank’s valuation at three times FY21 estimated book. Should the journey to achieving 18 percent RoE pans out, we expect the valuation gap to narrow.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.