Highlights:-- Volume growth will be critical to reviving revenue

- Intensifying competition remains a key threat

- Investors should take advantage of the price correction

-------------------------------------------------

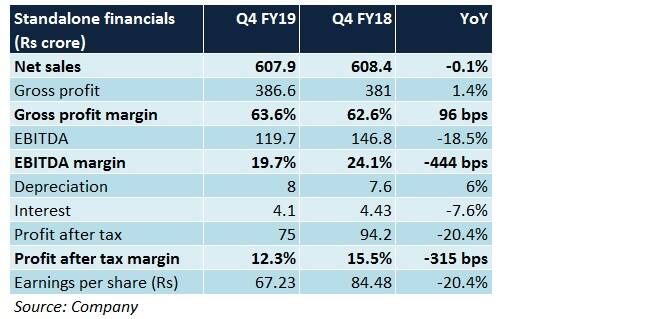

Page Industries reported a weak set of numbers for the quarter gone by, largely because of weak offtake by distributors/retailers, higher employee headcount and an increase in dealer incentives.

A combination of improved geographical coverage, new product variants, revival of volumes and higher garment capacities could help the company get its mojo back.

Page has the exclusive right to manufacture, distribute and sell innerwear- cum-leisurewear products under the 'Jockey' brand in India, Sri Lanka, Qatar, Oman, Bangladesh, Nepal and the UAE. It is also a licensed retailer of 'Speedo' swimwear products and accessories in India and Sri Lanka.

Q4 FY19 review

Positives

- Gross margin expanded due to stable yarn prices

Negatives

- Sales volume growth was only 1 percent year-on-year, whereas realisations were lower by 1.5 percent

- Employee costs and other expenses, as percentage of sales, rose noticeably year-on-year

- Lack of operating leverage and a higher tax rate caused bottom line margin to contract

Observations

Capacity expansion

In the next five financial years, Page's garment manufacturing capacity is slated to double from the current 260 million pieces per annum. While a new garment plant in Karnataka is likely to be commissioned in Q3 FY20, another one in Madhya Pradesh will be functional by Q4 FY21.

Network augmentation

As on March 31, Page's EBO (exclusive brand outlet) count stood at 620 and their contribution to yearly turnover was 16 percent. The objective is to increase the number of EBOs to 1,000 by FY21-end. The company's MBO (multi-brand outlet) count, totaling over 50,000 as of FY19-end, is estimated to grow on the back of foray into new markets.

New products

The headroom for growth in kidswear is significant, given the large population in India. Until now, Page has been primarily focussed on innerwear offerings within this segment. Going forward, products in the outerwear category may gain momentum.

Furthermore, athleisure and activewear products, which are high-margin by nature, would be high on the priority list in terms of launches.

The company's market share in the menswear segment is close to 20 percent. This, in itself, is a big positive worth capitalising on, since new products in the portfolio would already have a steady base of prospective buyers.

Going online

Considering the growing popularity of e-commerce portals and convenience shopping, the proportion of online sales to total revenue is anticipated to increase from 4 percent in FY19.

Outlook

The past

Historically, most of Page's top-line growth was value-driven on account of emphasis towards premium product variants. This was mainly because of Jockey's popularity among buyers.

Peers upping the ante

Intensifying competition from high-value brands of retailers such as Arvind Fashions and Aditya Birla Fashion & Retail would necessitate keeping prices in check. Therefore, volume growth -- and not value growth -- will become a crucial factor to monitor from now on. It also remains to be seen if the company can maintain its target of keeping margins in the range of 21-22 percent.

Trade not back on track

Subdued offtake from trade channels in the aftermath of the ongoing liquidity crunch is a challenge that could continue for at least a couple of quarters. Hence, it could be hard to achieve the desired 20 percent top-line growth target in FY20.

What should investors do?

An inability to sustainably deliver healthy volume-led growth, coupled with lack of market share gains in the smaller segments (womenswear, girls wear) in recent months, resulted in Page's de-rating.

After a weak Q4 show, the stock corrected sharply and is close to its 52-week low. At 41.6 times its FY21 projected earnings, Page continues to remain an expensive pick.

The ongoing consumption downcycle provides a valuable entry opportunity in beaten-down stocks. In our view, most of the downside seems to be factored in.

A change in product mix, gradual regularisation of trade sentiment, higher sale volumes (by way of enhanced capacities), large addressable audience (roughly 130 million consumers) and strong fundamentals should work in favour of the company in the long run.

Investors should, therefore, not overlook Page in spite of its heady valuation multiples. Having said that, the prospect of a re-rating anytime soon is unlikely and its rich valuation leaves no room to falter on volume growth and margins.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.