")

Madhuchanda Dey Moneycontrol Research

Karur Vysya Bank (KVB), the old Tamil Nadu-headquartered mid-sized private-sector bank, started the year with a subdued quarter, weighed down by significantly higher provisions as the last leg of corporate slippages came through on expected lines.

The bank’s business is gaining traction, while interest margins, still soft, show promise on the back of an improved deposit profile. Fees show traction and technology implementation is gathering steam under new CEO PR Sheshadri, an ex-Citibanker.

The only spot of bother from the earnings report is the high slippage from the commercial banking business. This is an area which would merit close monitoring.

We like the strategic initiatives of the bank and draw comfort from the end of asset quality woes in corporate banking.

The attractive valuation at 1X FY20 book and 1.3X FY20 adjusted book makes it an ideal accumulation candidate.

Subdued Q1FY19

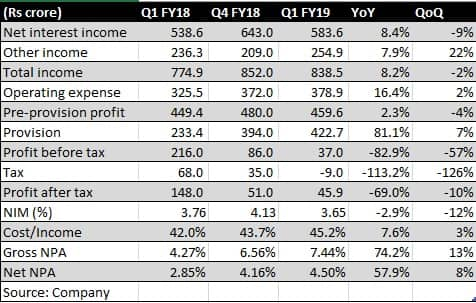

The decline in profitability in the first quarter of FY19 was attributed to a spike in provisioning as slippages remained high. The bank reported advances growth a tad better than the system and had softer interest margin resulting in 8.4% growth in its net interest income (difference between interest income and expense). Margin declined sequentially as the previous quarter had one off revenue receipt of Rs 60 crore. Management attributed interest reversals on account of spike in NPA (non-performing assets) as the reason behind softer margin.

The non-interest income component was supported by decent surge in core fees that rose 30% while treasury income was much lower. Operating expenses was elevated and the management mentioned the full impact of recent branch expansion contributing to the same. We expect the cost to income ratio to stay a tad elevated as the bank implements its strategy of technology adoption and employee addition in key functional areas.

NPA problem – is this the end of the road?

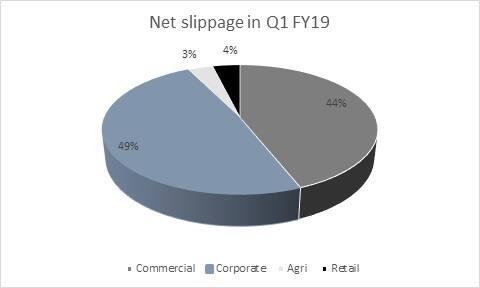

In Q1FY19, the bank saw gross slippage to the tune of Rs 785 crore and net of recovery the slippage stood at Rs 548 crore, similar to the level witnessed in the previous quarter. While the net slippage from the corporate book was on expected lines with much of the funded watch list and bulk of the standard restructured book slipping into NPA, the surprise was the high net slippage from the commercial banking book (CBG).

The bank attributed the CBG stress to difficulties faced by certain agriculture traders emanating from lower agri prices and impact on importers cash flow on account of LoU ban (letter of undertaking) as reasons and tried allaying concerns by pointing out that in past years there had been a spike in CBG slippage in Q1 which was almost equivalent to the slippage of next three quarters.

Source: Company

The bank guided to almost an end to asset quality woes from the corporate book as the outstanding troubled pool has dwindled to Rs 293 crore from Rs 663 crore in the previous quarter. The overall stress pool (including Security Receipts) is now 3.72% of total assets.

On the CBG side, the worst case slippage (if the same rate as Q1 continues) is expected to be an additional Rs 700 crore for remaining year although the bank realistically expects the slippage from this book to be Rs 300 crore. The management is hopeful of bringing down the slippage to a more normalised rate of 1.5 percent of advances. KVB is adopting an early alert system of troubled accounts to improve collection.

Efforts to de-risk the lending book

The bank has a diversified loan book and it is working towards increasing the share of its granular exposure through better adoption of technology. As of now home loan, loans against property, unsecured personal loan and working capital renewal is on the digital platform and the bank is likely to put CBG also on this platform which will enable better pricing of risk.

It is consciously bringing down the average ticket size of its corporate as well as commercial banking exposure. Internal risk management is being strengthened to improve the quality of the portfolio. The focus is clearly on risk adjusted growth and it expects a near-term growth in the mid-teens. In Q1FY19, the growth was a tad better than the system.

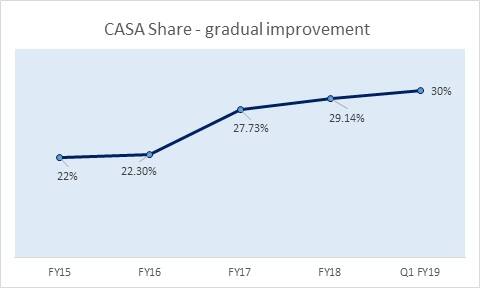

Commendable performance on CASA

The bank has improved its share of low-cost deposits (CASA) in a challenging environment where peers have lagged behind. While overall deposits grew by modest 5%, savings deposits grew by 13% leading to over 8% growth in CASA (low cost current and savings account) deposits. Consequently, CASA share has touched 30%. The management targets to take its CASA share to 31.5% by FY19 end and expects the roll out of digital banking and improvement in transaction banking to aid this effort.

While not explicitly guiding on margin, management expects MCLR (marginal cost based lending) based lending re-pricing to support lending yields and margin.

Source: Company

Adequate capital and reduced competition from PSU augur well

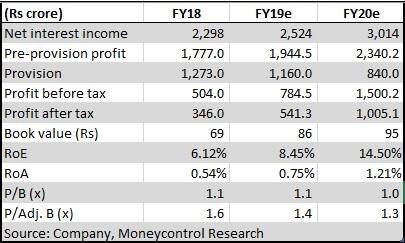

The bank has a healthy Capital adequacy ratio of 14.08% and seems well positioned to capture market share especially since PSU banks continue to vacate the market. We expect revival in earnings in FY20 riding on a much lower credit cost.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.