Neha Dave

Moneycontrol Research

- Liquidity scenario improving

- Interest rates are trending downwards

- Growth in affordable housing to continue outpace overall housing credit

- Aavas, a mid-cap affordable housing play, well poised for next leg of growth- High earnings potential makes Aavas a good long term bet

--------------------------------------------------

Housing finance companies (HFCs) have been at the centre of the market fall witnessed since September end. Stocks of HFCs nosedived following the funding concern. While higher interest rates were anticipated in FY19, HFCs were caught completely off-guard on the shrinking and in some cases completely withdrawal of liquidity triggered by defaults of IL&FS' group companies.

Once the Street’s favourite, investors now have shunned HFC stocks. This presents an opportunity amid chaos. The current environment is a good litmus test of overall quality for HFCs which will separate wheat from chaff. Handful of HFCs will not only survive but will also manage to flourish through this crunch. Aaavas Financiers will be one of them.

Aaavas, a mid-cap affordable housing play, is worth a consideration given that funding to NBFCs is rapidly easing out and interest rates are on a downtrend with 10-year G-sec yield falling almost 80 bps over the last 3 months.

High growth seen in affordable housing segment

We anticipate affordable housing segment to continue to grow at a high rate backed by the several initiatives of the government (interest subvention scheme, tax incentives, Housing for All by 2022, infrastructure status accorded to affordable housing, PMAY) along with regulatory push (priority sector status, lower risk weights on small ticket size loans).

We outline and explain the reasons as to why Aavas is an outlier in an overcrowded affordable housing space making it a worthy consideration.

Granularity of asset book and strong asset quality

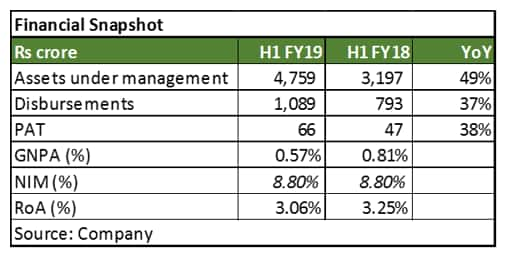

Aavas’s Rs 4,759 crore loan portfolio as at end September end grew 49 percent YoY. The encouraging part is that this growth has been volume driven and less reliant on expansion of average ticket size. Aavas’s average ticket size is around Rs 8.5 lakh and management intends to maintain it around the similar level (Rs 8-10 lakh).

Most comforting part is that has zero exposure to developer finance, under construction properties or land financing. Further, the company avoids lending to customers directly linked to agriculture and dairy activities as their cash flows are highly volatile. Such superior credit underwriting policies along with strong collection infrastructure and detailed analytics has helped Aavas build a relatively low risk loan book with gross NPA of 0.6 percent as at end September.

Having said, the company’s portfolio vulnerability remains high given a significant chunk of its loans is to self-employed customers as cash flows of borrowers in these segments are highly volatile. Despite this, we expect low credit losses given the secured nature of lending with moderate loan to value ratio at origination (around 50 percent), most of the properties being self-occupied and the company being covered under the SARFAESI Act.

Diversified funding mix

Aavas has a diverse funding mix with 87 percent of its borrowings are from term Loans, assignment, NHB refinancing and cash credit. Only 13 percent of its borrowings are from market with no borrowings by way of commercial papers. Putting simply, Aavas has negligible rollover risk which is the biggest concern faced by HFCs in a constrained liquidity environment.

Profitable growth

Despite the high growth, Aavas has been able to maintain superior profitability with return on assets of 3 percent in H1 FY19 mainly supported by healthy net interest margins and low credit costs.

Going ahead, margins could come under pressure as credit spreads have widened for HFCs. However, we expect the same to be partially offset by improvement in operating efficiency with increase in scale of operations. Hence overall, we don’t see much downside to earnings.

Aavas has more than adequate capital which improved further following IPO in October wherein it raised fresh capital of Rs 400 crore. Due to excess capital, return on equity (RoE) is depressed. We expect leverage to improve in medium to long term thereby increasing RoE.

Valuation undemanding considering high earnings growth potential

Affordable housing financing business requires a deep feet-on-street and a considerably evolved risk assessment processes, stringent underwriting norms, agile monitoring and superior collection mechanisms. With the usage of technology and analytics, Aavas has succeeded in creating all of these and build a superior franchise with significant competitive advantage.

At the current market price, Aavas is trading at 3.2 times FY20e book value. For a HFC with a strong earnings growth potential and ability to generate RoA between 2.5 percent - 3 percent, valuation seems quite reasonable.

On a relative basis also, valuations looks undemanding when compared to well-established financial lenders operating in retail lending space (Gruh Finance, Bandhan Bank). In the near term, we expect strong earnings growth to drive the stock price. In medium to long term, we expect valuation multiple to expand with scaling up of the franchise.

Given the high growth potential, experienced management along with a well-capitalised balance sheet, Aavas is well poised for the next leg of growth. It is a good long term bet available at reasonable price. Investors should buy the stock on dips.

For more research articles, visit our Moneycontrol Research page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!