Neha DaveMoneycontrol Research

Edelweiss Financial Services and IIFL Holdings, two of the fastest growing non-banking financial companies (NBFCs) in the country, reported robust earnings for the March quarter. Strong profit growth in both companies over the past five years is reflected in the stock’s performance. Edelweiss’s stock has grown 10 times in the past five years (generating 57 percent compounded annual return). IIFL’s stock is up 12 times in the same period, a return of 65 percent CAGR.

Given their superior performance, should investors look at these stocks incrementally and can do well going forward? Yes, in our view.

The fortunes of NBFCs are on an uptrend. Despite competition from private banks intensifying, NBFCs have gained share in the overall credit pie. In fact, they have identified and created a niche in certain non-traditional growth segments such as structured credit, wealth management and distressed asset. IIFL and Edelweiss, with diversified business segments, have unique growth drivers and remain key beneficiaries of increased penetration of financials services

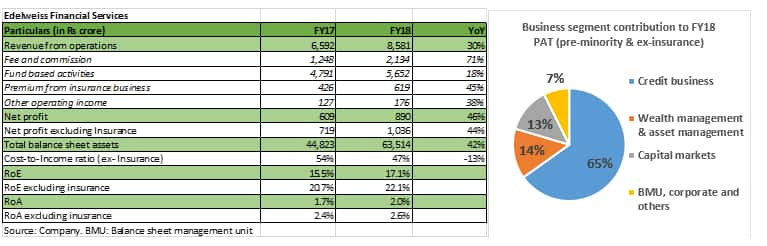

Edelweiss Financial Services: FY18 at a glance

The company reported robust FY18 earnings with net profit surging 46 percent year-on-year (YoY) on the back of strong credit growth and increased scale of the wealth management business.

At Rs 42,010 crore, its credit business is the key revenue and profit driver, contributing 65 percent of consolidated profits (pre-minority interest and excluding insurance).Retail (39 percent of credit book) and corporate (46 percent) grew 81 percent and 41 percent YoY, respectively.

Edelweiss operates the largest asset reconstruction company (ARC) in India, with a book size of Rs 44,100 crore. The business can potentially generate an internal rate of return (IRR) in the 17-18 percent range.

Performance of the wealth and asset management businesses continued to remain splendid. Assets under advice (AuA) swelled to Rs 90,100 crore, an increase of 49 percent YoY. Net new money flow stood at Rs 15,100 crore. The asset management business comprising mutual funds and alternative assets saw a 60 percent YoY growth to Rs 29,200 crore.

Its institutional broking and investment banking arm reported strong performance, but remains susceptible to inherent volatility in capital markets.

The company’s life insurance joint venture with Tokio Marine Insurance has been incurring losses and remains a drag on the group’s overall profitability.

The cost-to-income ratio of the overall business has improved to 60 percent compared to 67 percent last year. The company reported return on assets (RoA) and return of equity (RoE) of two percent and 17.1 percent, respectively. Excluding insurance, RoA and RoE stood at 2.6 percent and 22.1 percent, respectively.

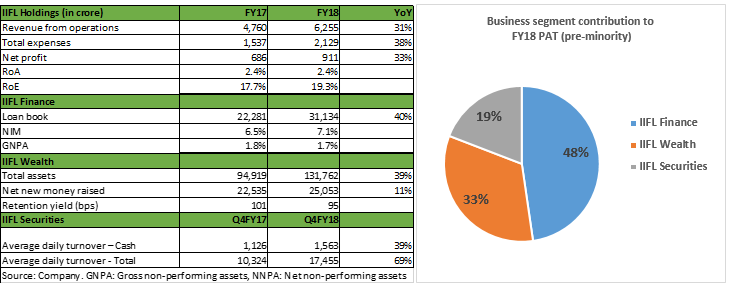

IIFL Holdings: FY18 snapshot

The company reported a 33 percent YoY growth in FY18 consolidated profit after tax (PAT) after minority interest at Rs 911 crore. Profit growth was strong across each of its core businesses: IIFL Finance (loans and mortgages), IIFL Wealth (wealth and asset management) and IIFL Securities (equities, investment banking, and commodities).

IIFL Finance: Its lending arm posted profit growth of 31 percent YoY on the back of a 40 percent growth in loan book to Rs 31,134 crore and 60 bps expansion in net interest margin (NIM) expansion to 7.1 percent. Its loan book is well diversified and predominantly retail. In fact, 40 percent of its loan book is priority sector lending (PSL) complaint.

IIFL Wealth: The company posted robust profit growth of 54 percent YoY as total assets managed surged 39 percent YoY to Rs 131,762 crore. The retention yield on fee-based assets was 71 bps and likely to be in the 65-70 bps range going forward.

IIFL Securities: IIFL is a key player in both the retail and institutional segments with a four percent share in daily cash turnover. Profit growth in the segment was 41 percent YoY due to buoyant capital markets.

At a consolidated level, IIFL delivered RoA and RoE of 2.4 percent and 17.7 percent, respectively.

Outlook and recommendations

Edelweiss has evolved into a ‘bank-like’ structure, with diversified revenue streams from its earlier capital market focused business. Further, it has carved out a niche in certain segments like distressed assets. It is rapidly gaining scale in the wealth management space and is among the top five players in that segment.

Similarly, IIFL Holding is present across multiple lines of lending without any identifiable niche but is a market leader in the wealth management space.

We see profitability improving for both these NBFCs on the back of strong growth in the lending book, buoyant capital markets and steady wealth/asset management businesses.

While there are multiple growth drivers, it is the non-lending/fee-based business in general, and wealth management business in particular, that excites us the most about both franchises. Since the wealth business does not require additional capital, it can potentially generate non-linear profit growth and RoE expansion. Also, revenue streams from wealth management are less cyclical and can provide cross-selling opportunities. Outlook for the wealth management sector is promising as the market is underpenetrated, likely to grow in sync with India’s economic growth and rising income levels in the economy. The void created by the exit of a few foreign banks in the wealth space is being smartly captured by IIFL and Edelweiss.

Though the performance of both NBFCs has been resilient so far, investors should be cognisant of the inherent risks as well. The lending book of both companies are relatively unseasoned. Edelweiss’s structured credit and real estate financing segments and IIFL’s retail book needs to be tested through business cycles.

Additionally, Edelweiss’s performance in the distressed asset segment is vulnerable to any delay or inability in the resolution of delinquent assets and capital availability. Going forward, we see this segment potentially providing strong carry income if it can acquire operating assets at adequate haircuts. Canada’s second largest pension fund, Caisse de dépôt et placement du Québec’s (CDPQ) 20 percent stake in the ARC business gives us comfort on the capital adequacy front.

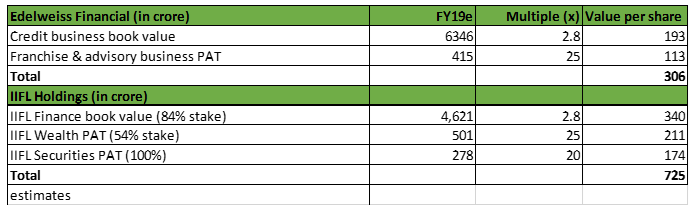

On the valuation front, both stocks seems fairly priced with lending book at 2.8 times one- year forward book value (P/BV) and wealth franchise at 25 times one-year forward earnings (P/E) . Given the sectoral tailwinds and multiple growth levers, investors with a long-term horizon, wanting to participate in a high growth, diversified financial services companies can consider these stocks.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!