With the Union Budget barely a month away, a section of the market will be eyeing tactical bets that could pay off if some of the policy expectations come through.

These 10 stocks are likely to be in focus in the countdown to the Budget 2023:

Infrastructure

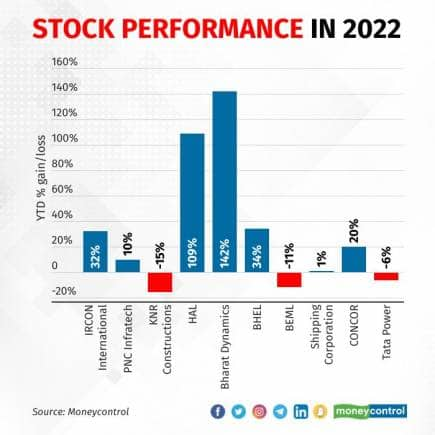

With the government continuing to focus on infrastructure, stocks like IRCON International, PNC Infratech and KNR Constructions could be in the limelight

Besides, decent growth visibility because of a likely increase in railway capital expenditure has also boosted sentiment for the sector in general.

It is widely expected that the government will allocate more funds to the roads ministry to speed up construction to more than 50 km of highways daily.

This wholly-owned subsidiary of Indian Railways is an engineering and construction company that specialises in major infrastructure sectors including railways, highways, bridges, flyovers, tunnels, metros and railway electrification.

“IRCON International Ltd being one of the major players in infrastructure sector is likely to benefit from the government’s opportunities in the sector,” HDFC Securities said.

The company’s order book as at September 2022 stood at Rs 40,020 crore. The order book comprised 77 percent from the Railway segment, 18 percent from Highways, and 5 percent from other segments respectively, according to the brokerage firm.

Despite strong competition, the company’s strong revenue visibility has made investors confident.

The company had a muted order inflow during the first half of FY23, but is looking at execution in this particular year rather than targeting order inflows as it believes that the existing order book is very healthy for four-five years of revenue, HDFC Securities pointed out. The company still aims to secure new orders amounting to Rs 8,000-10,000 crore during the current financial year, it added.

Two brokerage firms that track the stock have a ‘buy’ recommendations on IRCON International shares, according to Bloomberg data.

PNC Infratech & KNR Constructions

PNC Infratech and KNR Constructions are on Nomura’s buy list in the infra sector, as both companies have been consistently generating operating cash flow and reducing debt.

Nomura likes PNC Infratech as the company has succeeded in turning its net debt to net cash. At KNR Constructions, successful asset sales have led to the company having one of the strongest balance sheets in the sector.

Healthy order book of about Rs 193 billion in the second quarter, stellar execution pace and most projects getting completed within stipulated time, along with stable operating margins of 13‐14 percent and low debt‐equity are some positives for PNC Infratech, multiple analysts believe, while Motilal Oswal Financial Services said that the tender pipeline appears to be strong for KNR Constructions which should ensure decent order wins in FY23.

According to Bloomberg data, 20 brokerage firms have a ‘buy’ rating on PNC Infratech, and 22 brokerages have a ‘buy’ rating on KNR Constructions.

Defence sector

Healthy order books and the government’s push for localisation have led to many wealth managers turning bullish on defence stocks. Plus, expectation that the government might announce some more measures for indigenisation have spurred buying in defence stocks.

Hindustan Aeronautics Ltd (HAL) is the largest defence public sector undertaking (PSU) in India, which is engaged in design, development, manufacture, repair, overhaul, upgrade and servicing of a wide range of products, including, aircraft, helicopters, aero-engines, avionics, accessories and aerospace structures.

It has a healthy order book position as of September 2022 at Rs 83,800 crore, which is around 3.2 times trailing 12-month revenues.

HAL expects the order book to increase by Rs 500 billion in the next six months through manufacturing orders.

Analysts like the company for its healthy order book and a robust order pipeline which makes them confident about healthy and consistent revenue and earnings growth.

All nine brokerages covering HAL have a ‘buy’ call on the stock.

The company is one of the leading defence PSUs in India which is engaged in the manufacture of surface to air missiles, anti-tank guided missiles, air to air missiles, underwater weapons, launchers, countermeasures and test equipment.

The company’s order book is expected to grow two times to Rs 250 billion in the next two-three years.

Bharat Dynamics is expected to see a sharp jump in order book on the government’s increasing thrust on indigenous missile development program.

Antique Stock Broking, in its report dated September 1, 2022, said, “Exports, which is 5 percent currently, has the potential to grow meaningfully as the Cabinet Committee on Security has approved export of Akash missiles to nine countries.”

As of September 2022, the company’s order book stood at Rs 12,000 crore.

Seven brokerage firms have a ‘buy’ recommendation on the stock, while one says ‘sell’, Bloomberg data pointed out.

Bharat Heavy Electricals Ltd (BHEL) is India’s largest engineering and manufacturing enterprise in the energy and infrastructure sector. It is a leading power equipment manufacturer globally and has major offerings for industry and infrastructure sectors, including transportation, defence and aerospace, renewables, transmission, industrial products, energy storage solutions and new business areas like electric vehicles (EVs).

It has also established itself as a leading engineering, procurement and construction (EPC) player in the floating solar passenger vehicle (PV) segment of the domestic market.

ICICI Securities is of the view that sustainable profitable growth is likely for BHEL. Addition of new orders, along with favourable payment terms, could help execution gather pace, followed by margin improvement. Recent correction in commodity prices might also better profitability. All these, coupled with BHEL’s efforts to improve cash flow and reduce receivables are key positives.

The company’s order book now stands at approximately Rs 1.06 trillion, which is 4.6 times trailing 12-month sales, according to ICICI Securities.

Order inflow in the second quarter of FY23 was robust at Rs 120 billion. The company’s management highlighted revival of the thermal order pipeline with around 5 GW of expected annual ordering for the next five years while order intake for the industrial segment was up 78 percent year-on-year (YoY) to Rs 22.8 billion.

Some analysts believe the company offers decent earnings growth at a reasonable valuation.

According to Bloomberg data, 16 brokerage firms have a ‘sell’ rating on the company’s stock, whereas two have ‘buy’ and three ‘hold’.

Divestment

With the government divesting part of its stake in the company, there is an expectation that the upcoming Union Budget might have some announcements on the schedule for the stake sale.

The Bengaluru-based company serves sectors like defence, railways, power, mining and infrastructure.

“We believe BEML is the biggest beneficiary of the ongoing metro capex in India, with market leadership in metro coaches,” said Reliance Securities in the latest result update. With rapid increase in demand for urban mass transportation systems in the country, several metro rail projects are in progress to improve intra-city connectivity, it added.

BEML is one of the companies that is lined up for divestment. The conclusion of strategic sale of the company is said to spill over to the next fiscal.

Currently, the government’s shareholding in BEML is 54.03 percent. In 2016, the Union Cabinet approved strategic disinvestment along with transfer of management control of the company.

Two brokerage firms have ‘buy’ recommendation on the stock, whereas one says ‘sell’.

Another company that the market is keenly tracking is Shipping Corporation Ltd (SCL), as it is among the candidates queued up for divestment.

The approval from the Ministry of Corporate Affairs for non-core asset demerger for SCL is expected this month, as per a report. It takes about two months from approval to list the demerged entity, following which bids for the company would be invited, the report said.

The government is selling 63.75 percent stake in SCL along with management transfer. In March 2021, it had received multiple bids for buying the stake in SCL, but the demerger process got delayed.

In May 2022, the board of SCL approved an updated demerger scheme for hiving off the non-core assets of the company to Shipping Corporation of India Land and Assets.

Container Corporation of India

Container Corporation of India (CONCOR) is a dominant player in the container terminal operator business commanding 65 percent market share with around 60 terminals.

The management has guided for clocking 6.5-7 million twenty foot-equivalent unit (TeU) volumes in the next three to four years (currently at four million TeUs) and subsequently doubling revenues, ICICI Securities pointed out. Further, various newer initiatives are expected to diversify the company’s offerings to customers, and thereby capture higher wallet share, it said.

Including the upbeat business prospects, there are a few other triggers for the stock to climb higher, analysts believe. One of these is privatisation.

As per a news report, the government may invite expressions of interest (EoI) for strategic disinvestment of CONCOR in January, a senior official was cited as saying. This will mark the beginning of the process of government selling its shareholding to private firms, the report added.

The Centre currently owns 54.8 percent stake in CONCOR. The Cabinet Committee on Economic Affairs had, in November 2019, approved the strategic divestment of government equity of 30.8 percent, along with the transfer of management control to a strategic buyer.

As per another report, JSW Group, Maersk and Essar Ports have shown interest in bidding for CONCOR.

Of the brokerage firms that track CONCOR, 20 have recommended ‘buy’, six have said ‘hold’, while another six have suggested ‘sell’.

Renewables

To combat climate change, several countries across the globe, especially India, are turning to renewables, such as solar and wind.

Recently, Union Minister of Power and New and Renewable Energy RK Singh, said to boost the production of renewable energy, India will have more than 65 percent power generation capacity from non-fossil fuels by 2030.

Renewables was one of the emerging themes that Anand Shah, Head - PMS & AIF Investments, ICICI Prudential Asset Management Company, had pointed out recently.

Even Deepak Jasani of HDFC Securities is of the opinion that defence and renewable stocks could bounce up faster than others in 2023 given the visibility of revenue and margin growth in these two.

Tata Power is among the country’s largest integrated power companies.

According to ICICI Securities, the long-term potential of the company's businesses is good, especially the renewables and distribution businesses. “We also believe TPWR (Tata Power) is the best-placed private player in the power sector, with businesses across the value chain and backward integration,” the brokerage firm added.

The company is aiming for more divestments in the next 12 to 24 months after inducting new investors into its renewable energy business, Managing Director and Chief Executive Officer, Praveer Sinha, told Moneycontrol in November.

As per Bloomberg data, 10 brokerage firms have a ‘buy’ rating on the stock, while another 10 have a ‘sell’ rating, and only four have recommended ‘hold’.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.