Shubham Agarwal

March F&O series turned out to be one the most brutal expires of recent memory, as major indices sawed-off 20 percent. The uncertainties revolving around COVID-19 wiped out nearly 4,000 points from Nifty50 during the month's low, but some recovery in the last week helped the index settle 3,000 point lower on expiry to expiry basis.

The open interest tally for the entire population of underlying dropped. More than the directional impulse the fear was the guiding force of this shrinking participation. Index futures that are usually resorted to as a hedge against down moves also fell victim to the fear of the unknown as both Nifty and Bank Nifty futures lost 26 percent and 35 percent in OI (Open Interest) respectively.

If we come to the stock futures OI tally, none of the sectors saw any increment in OI. Traders losing courage in the large swings were evident in this expiry as the rollover percentage in most of the stocks and sectors were not so low despite that the post expiry OI went down drastically. This was primarily due to the fact that the swings prior to expiry have pushed out most of the participants out of their respective trading bets.

Slicing it down further, FMCG was overwhelmed by the drop in Price and OI in ITC but there were stocks like DABUR, PIDILITE that had long additions during expiry and should have carried forward. IT was the sole sector in March expiry to have OI additions but that too due to short interest into INFY and largely in TCS. Metal stocks had one out of ordinary addition of short interest in VEDL, also DIVISLAB among pharma stocks added longs early on March which seems to have rolled over.

On the sentimental front, the implied volatility reached a record high this expiry overshooting the 2008 levels also. The event at this juncture the implied volatility remains high with India VIX at an unprecedented level of 70.

As far as option composition is concerned Nifty Open Interest Put Call Ratio at the end of this week was at 1.2. This was because of a combination of factors. The Put writers caught on a wrong foot due to the fall and writing in deep out of the money Puts due to the very expensiveness of Nifty Options. For example, a 2500 points lower Put is trading at Rs 100, which in a normal situation would be worth Rs 0.05.

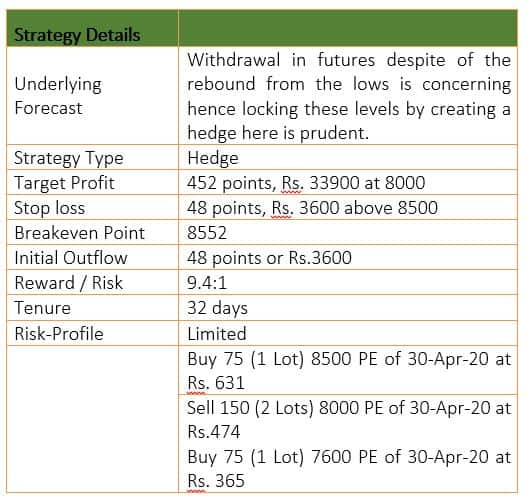

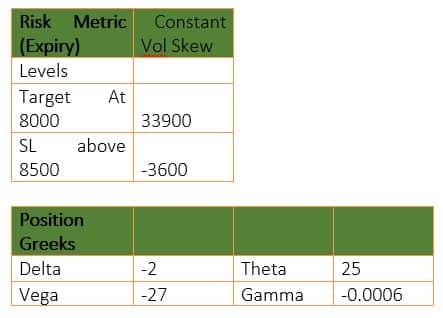

At this juncture, level of fear appears still high led by the unknown ultimatum of the on-going pandemic. Withdrawal in futures despite the rebound from the lows is concerning, hence, locking these levels by creating a hedge here is prudent.

The only way to trade downside is by creating a limited drawdown strategy hence butterfly is advised. Since the depth of the market is unknown, modification by bringing the lower strike up by 100 points is done to keep the strategy profitable at all lower levels.

Modified Put Butterfly is a 4-legged strategy where 1 lot of Put close to current underlying level is bought against that 2 lots of lower strike Puts are sold and 1 more lot of Put is bought but closer to the Put sold strike. This keeps the lower but constant profits in case of downward breakout. This is a fairly risk-averse and a universal strategy.

(The author is CEO & Head of Research at Quantsapp Private Limited.)

Disclaimer: The views and investment tips expressed by investment experts on moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.