Over the past few weeks, Finance Minister Nirmala Sitharaman has spoken at a number of events, an unusual occurance given that the Union Budget 2020-21 is just six weeks away and the budget-makers usually go into radio silence in the months leading upto the event.

Also, the finance minister has been dropping tantalising hints on what the budget may contain as the COVID-19 pandemic-hit economy begins its slow path to recovery.

On December 18, at an event of industry body Confederation of Indian Industry (CII), Sitharaman said the upcoming budget will be unlike anything presented before. “Send me your inputs so that we can see a Budget which is a Budget like never before, in a way. 100 years of India wouldn't have seen a Budget being made post pandemic like this,” she had said.

In virtual appearances before that, Sitharaman publicly said the budget will see a massive public sector investment and expenditure push, including on infrastructure projects and the health sector.

“We shall definitely sustain the momentum of public spending in infrastructure. Because that is the one way we assure that the multipliers will work and the economy's revival will be sustainable. I am conscious that the forthcoming Budget will have a vibrancy that is so required for the economy's revival, sustainable revival," she had said on December 15.

None of Sitharaman’s immediate predecessors, including the late Arun Jaitley, stand-in Piyush Goyal, or P Chidambaram, were known to publicly reveal as much before their budgets.

But then, we are living in unprecedented times, and Sitharaman, through her public statements, seems to be preparing the markets, banks, and ratings agencies for an unprecedented budget.

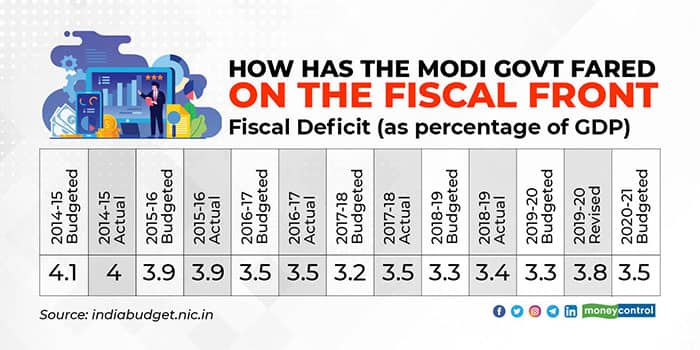

Since 2004, the Fiscal Responsibility and Budget Management (FRBM) Act has guided the making of the Centre’s budget. The FRBM Act has for long maintained a medium-term fiscal deficit target of 3 per cent of gross domestic product (GDP). This target has never been met and keeps on getting postponed every year. The medium-term target in the 2020-21 budget is for a fiscal deficit of 3.1 per cent of GDP by FY23.

The COVID-19 pandemic and its impact on the Indian economy has put to rest any hopes of meeting this target. In fact, by all indications, the Union Budget 2021-22 may push back that target by another five years or so.

Jaitley used to visibly pride himself with reining in government finances and bringing fiscal discipline into the budget making process. And as the chart shows, the Narendra Modi government succeeded to a large extent.

The fiscal deficit came down from 4.5 per cent of GDP in the United Progressive Alliance (UPA) government's last year to 3.4 per cent in FY19. Then things got difficult as the Indian economy underwent a slowdown in 2019, even before the pandemic.

Now, the Prime Minister and the government will have to let go of fiscal conservatism.

The government is planning a massive public spending boost which will centre on economic revival and employment creation post-COVID. What is certain that the upcoming budget will have the highest ever capital expenditure outlay from the central government and could easily cross Rs 6-7 lakh crore.

For FY21, the Centre had budgeted its own capital expenditure at Rs 4.13 lakh crore, which has been increased by Rs 35,200 crore, announced by Sitharaman in October and November as part of the various Aatmanirbhar Bharat packages.

The 15th Finance Commission is learnt to have recommended a fiscal deficit target range for each year of its award period, till FY26, instead of a single number. The fiscal deficit for this year is expected to be around 7.5-8 per cent of GDP, and could be the Centre’s starting point of a fiscal roadmap going ahead.

The fiscal deficit target for the current year was budgeted at 3.5 per cent of GDP. That target no longer holds as the COVID-19 pandemic has led to dwindling revenues and higher expenditure commitments for the central government.

Apart from capital expenditure, the upcoming budget is also expected to substantially increase the outlay for grants for creation of capital assets, health expenditure and money to states under certain schemes. A one-time provisioning for COVID-19 related expenditure could be as high as Rs 80,000 crore.

In normal times, the biggest effect of a burgeoning fiscal deficit is higher borrowing and wider debt-GDP ratio. However, the Centre is not concerned on that front for next year. An expected GDP contraction this year means a low-base effect for next year, which will lead to debt-GDP consolidation.

This is what the finance minister seems to be preparing the markets for. A budget with never before seen fiscal slippage and public spending outlay.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.