Neha DaveMoneycontrol Research

Highlights

- Healthy loan growth aided by domestic retail loans

- De-risking of asset book continues while building an enviable liability franchise

- Slippages continued to trend downward

- Credit cost to decline sharply from FY20

- Valuations compelling; rerating to continue --------------------------------

The third-quarter earnings of ICICI Bank strengthens our belief that the bank is well on track on multiple fronts to deliver to targeted returns by June 2020. In fact, we will not be surprised if it revises targeted consolidated RoE (return on equity) of 15 percent upwards in another couple of quarters.

ICICI Bank reported a very healthy performance for Q3 FY19 with core pre-provision operating profit (excluding treasury income ) increasing by 14 percent year on year (YoY). However, rise in provisions led to muted headline number of reported net profit declining by 3 percent YoY.

With bulk of problem assets already recognised till FY18 and in Q1 FY19, the slippages or gross additions to non-performing assets continued to trend downward in Q3. However, our enthusiasm for the bank is not just limited to receding asset quality problems. There is more than a reason that makes us decisively positive on the stock.

The bank has continued to improve its retail franchise – both assets and liabilities. ICICI Bank’s balance sheet it is now comparable to best in class and is the first reason for our optimism with bank’s CASA (low cost current and savings) deposits at 49 percent and retail loans at 59 percent of total loan book.

Bank’s adequate capitalisation is the second reason that makes us affirmative. In an environment where large a large part of the lending system has been crippled because of a shortage of capital (public sector banks) and receding liquidity (NBFCs), ICICI Bank is well poised to leap ahead with more than adequate capital.

Third and the most important reason is expectation of improvement in return ratios. With the receding asset quality issues and provisions thereof, we expect the reported numbers to improve significantly from FY20 as the current year (FY19) remains a year of consolidation due to higher credit costs.

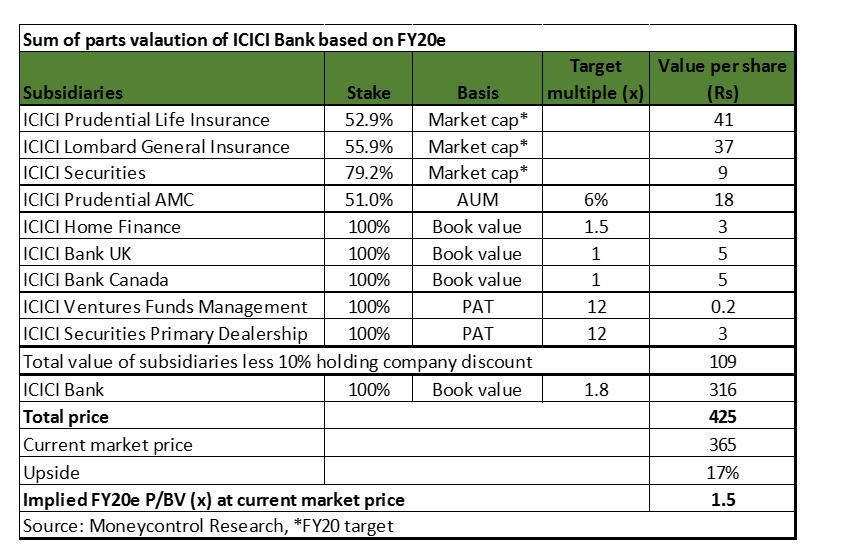

And last but not the least, considering multiple levers that should help drive sustained improvement in RoE, bank’s valuation is extremely attractive. With the stock currently trading around 1.5 times FY20e book, current valuations seems to be pricing in the most concerns and offers a favourable risk reward.

Key positives

Overall advances growth stood at 12 percent YoY as healthy 14 percent growth in domestic loan book was partially negated by 5 percent de-growth in international loans. A strong focus on retail lending has enabled ICICI Bank to grow its domestic loan book almost in line with the system growth, despite cyclical weakness in the large corporate segment. Retail assets grew by solid 22 percent YoY while corporate loans were almost flat YoY.

The net interest margin (NIM) for the quarter improved to 3.40 percent from 3.33 in previous quarter mainly due to better margins on international book while margins on the domestic book remained almost stable at 3.72 percent.

Fee income growth was healthy at 16 percent driven by retail fees which constituted 73 percent of total fees.

Provision coverage ratio (PCR) improved significantly to 68.4 percent (up 950 bps sequentially). This is much faster -than-expected acceleration in bank’s earlier stated objective to improve PCR to 70 percent by June 2020.

Gross slippages to non-performing assets declined in Q3 to Rs 2,091 crore which was very encouraging. Thanks to contained slippages and higher provisioning, net NPAs declined to 2.58 percent compared to 3.65 percent in Q2.

The bank’s exposure to list 1 and list 2 of corporates undergoing resolution through National Companies Law Tribunal (NCLTL) declined at Rs 3,816 crore and Rs 8,828 crore respectively. PCR on the list 1 and 2 was very healthy at 90 percent and 72 percent respectively as at end December increasing the likelihood of write backs in future.

Additionally, the bank’s disclosed pool of loans to corporate and SME rated BB and below (potential stress) declined to Rs 18,812 crore (equivalent to 3.3 percent of the loan book) which also include the IL&FS exposure.

Key negatives

CASA (low cost current and savings accounts) ratio dipped marginally to 49.3 percent as at end December as growth in CASA deposits lagged growth in term deposits. Still overall performance on liability continues to be impressive.

Current stock price factors in known issues; valuation rerating to continue

In May last year, management articulated its strategy to deliver consolidated RoE of 15 percent while improving NNPA to 1.5 percent and maintaining provision cover above 70 percent by June 2020.

With its 2020 vision in place, investors should expect much lower NPA formation and normalised credit cost in FY20, mid-teen loan growth, steady margin and a fast journey to reach RoE of 15 percent. With a strong capital adequacy (Tier I capital ratio at 15.14 percent), we don’t see many constraints in delivering its targets.

With a potential improvement in return rations, the current valuation of its core book at 1.5 times FY20e P/BV looks compelling. In fact, ICICI bank is trading at significant discount of more than 30 -40 percent relative to its closest corporate lending peer having similar asset quality issues.

The indictment of Chanda Kochhar by internal enquiry committee doesn’t alter bank’s growth plans. Appointment of Sandeep Bakshi as CEO had lifted the cloud of management related uncertainty. Q3 earnings indicate a clear sky making ICICI Bank an exciting yet relatively safe investment bet for long term.

For more research articles, visit our Moneycontrol Research page.

Moneycontrol Research analysts do not hold positions in the companies discussed here.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!